One of the biggest enduring myths in the financial markets is the distinction between public and private markets, and the article of faith that private markets should be lightly regulated. The time may have come to question this article of faith.

The issue has become a topic of interest in light of the turbulence being faced in the private credit markets, and also the steps in the US and elsewhere to allow public funds to invest in alternative assets. It is also important, given the growing share of private capital markets, amplified as it is by the secular decline in interest rates (in turn a consequence of several factors, including ageing populations, financial market integration, and globalisation).

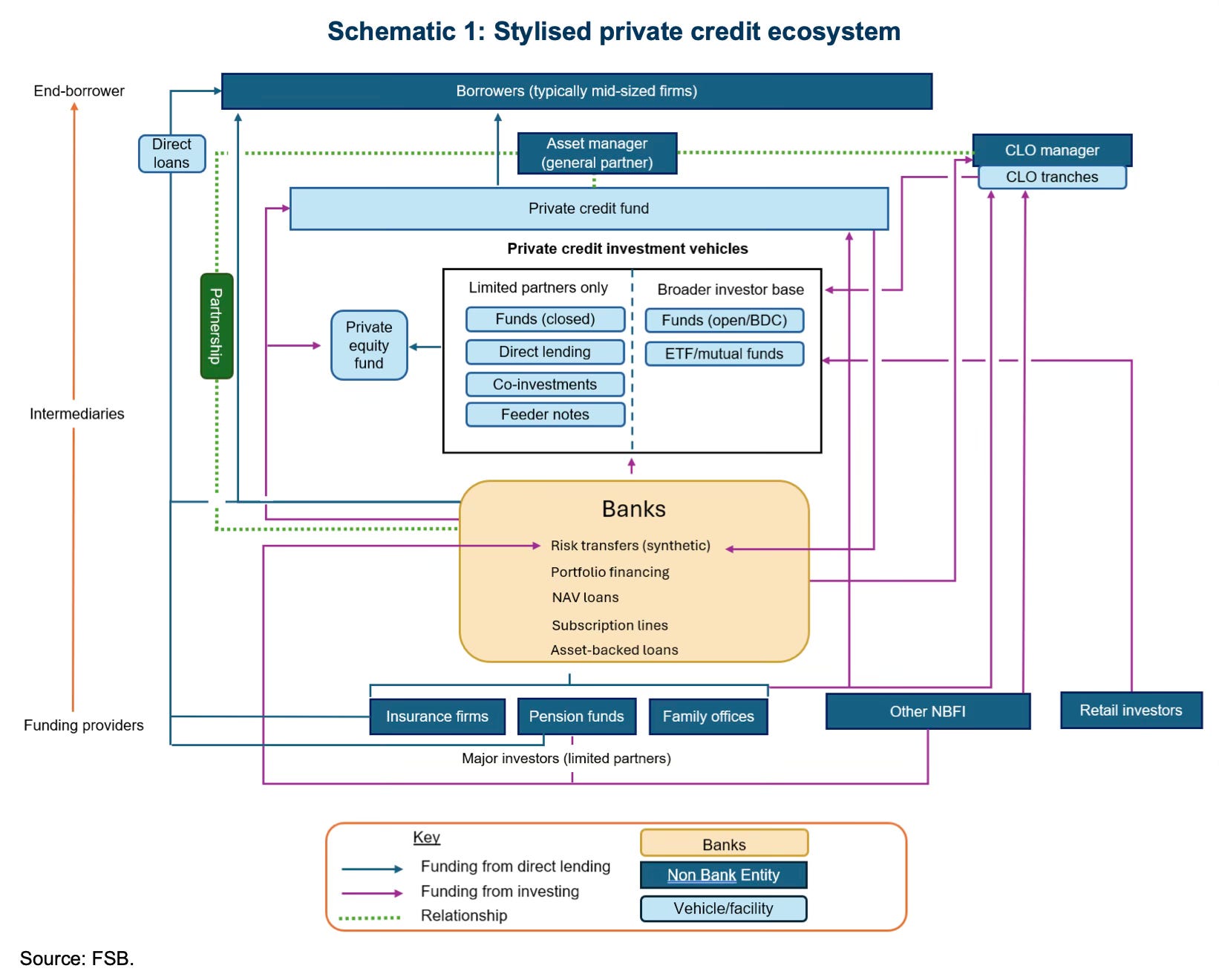

On the former (private credit markets), the FSB has just published a report on private credit, pointing to several vulnerabilities arising from complex interlinkages with banks, borrower credit quality concerns, and valuation opacity.

This activity has grown rapidly, to an estimated $1.5-2.0 trillion in assets at end-2024 and is heavily concentrated in a few jurisdictions… Banks and private credit funds are connected through financing arrangements and strategic partnerships. Across FSB members, the available data captures direct exposures of around $220 billion of drawn and undrawn bank credit lines to private credit funds, while some commercial estimates range from $270-$500 billion… there are also potential vulnerabilities from a range of other indirect exposures including through banks providing revolving credit facilities to companies that are simultaneously borrowing from private credit funds and the growing use of synthetic risk transfers.

The former Bank of England Governor, Andrew Bailey, writes,

Private credit has significant interlinkages with banks, asset managers, insurers and private equity. These multiple layers of leverage across the ecosystem deserve deeper scrutiny. While direct bank exposure to private credit funds may be limited, indirect connections are extensive. Banks are establishing partnerships with asset managers that have a credit focus and often provide revolving credit facilities to companies simultaneously borrowing from private credit funds. Insurers actively invest in private credit markets while also establishing indirect connections to private credit through participation in reinsurance arrangements. Private equity managers increasingly own the insurance companies. These interlinkages can be difficult to detect, assess and manage — and so can the related risks.

On the latter (public financial institutions’ exposure to private markets), in August 2025, President Trump signed an executive order directing regulatory agencies to reexamine existing regulations and open the $9 trillion US retirement market to cryptocurrency, private equity, and other assets like property. Following this, on March 30, 2026, the US Department of Labour issued orders allowing 401(k) plans easier access to alternative assets.

So why are private capital markets lightly regulated?

The standard response is that they are targeted at sophisticated, institutional investors who are presumed to have the ability to conduct their own due diligence and bear the risks, including high illiquidity. To this extent, it is argued, they do not pose the kind of negative public externalities and systemic risk that is associated with institutions that are public-facing (which take deposits, savings, premiums, etc., from retail investors). Any losers are those well-heeled investors who have the ability to absorb their losses.

Is it really the case? What does the evidence inform us?

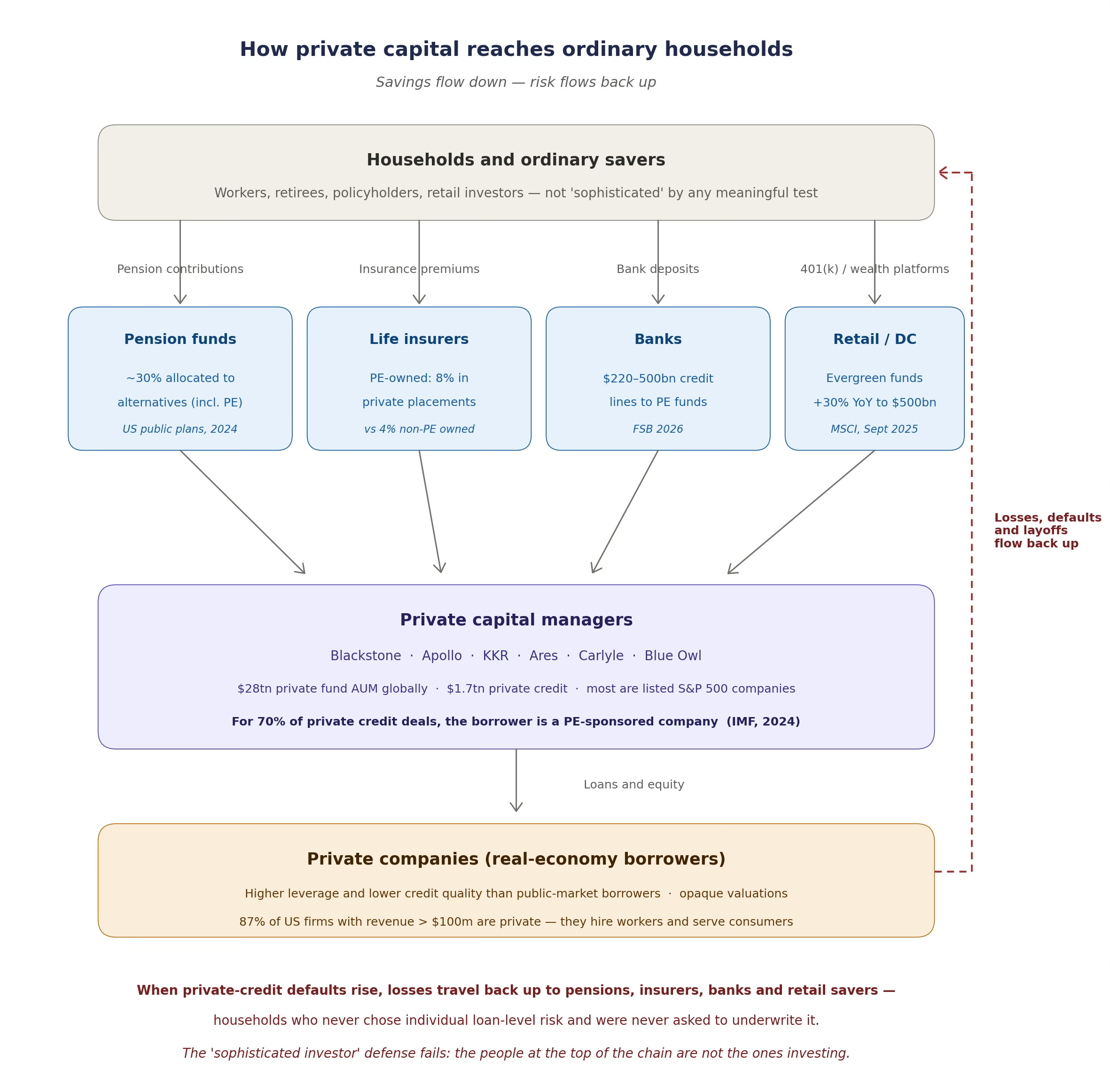

The reality is, as the following figures and statistics show, that retail investors are increasingly participants, both directly and indirectly, in the private capital markets. Here is a simple illustration of the channels of exposure of public-facing financial institutions to the private capital markets.

What makes this arrangement questionable is that the people at the top of the chain, the actual end-bearers of the investment risk, are not the ones doing the investing. Whatever counts as "sophistication" sits with the agents in the middle layer, not the principals at either end. However, the costs and consequences are borne primarily by the capital providers.

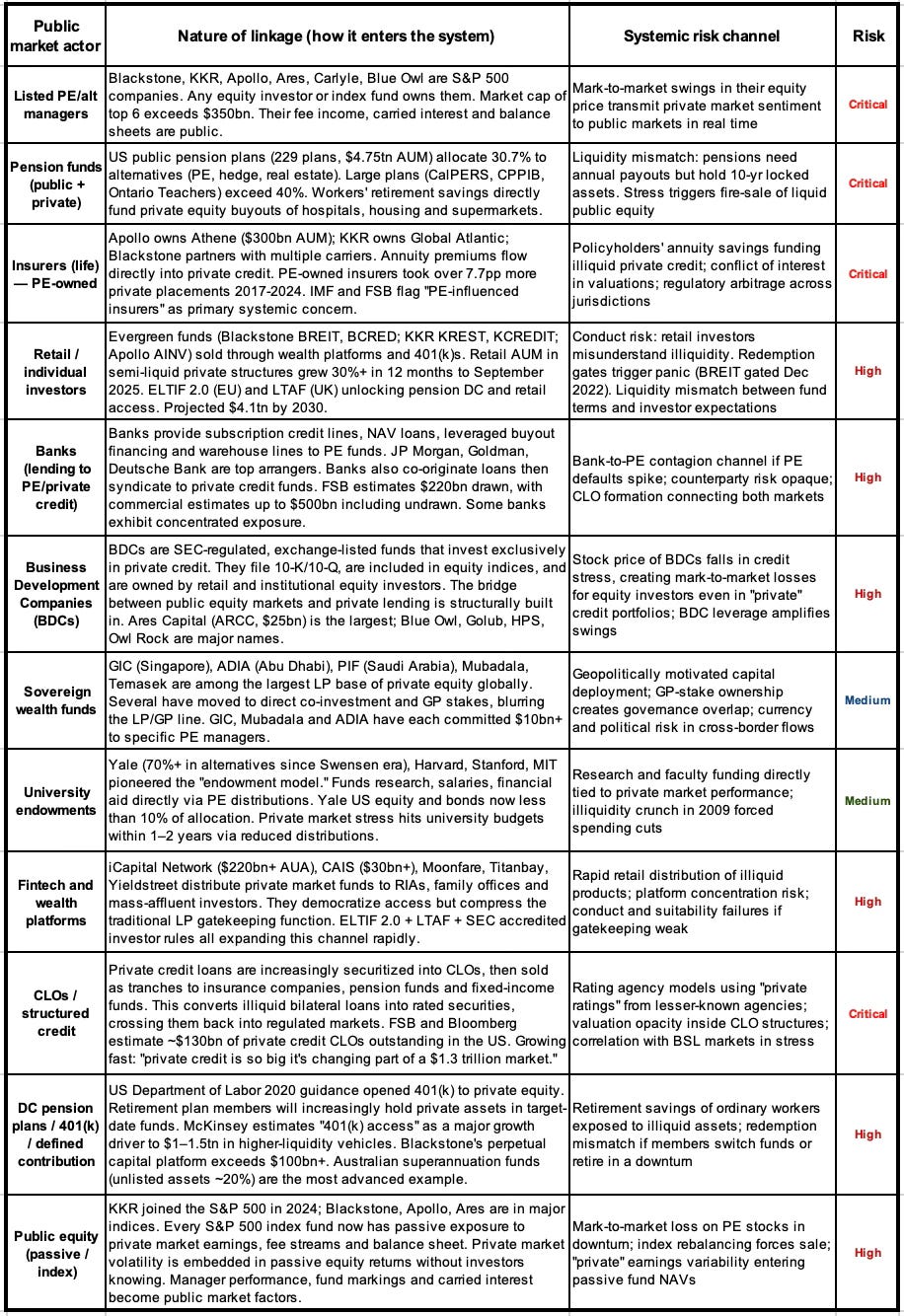

The table below is a summary of the various institutional investors, their respective linkages to the private capital market, and their systemic risk channel.

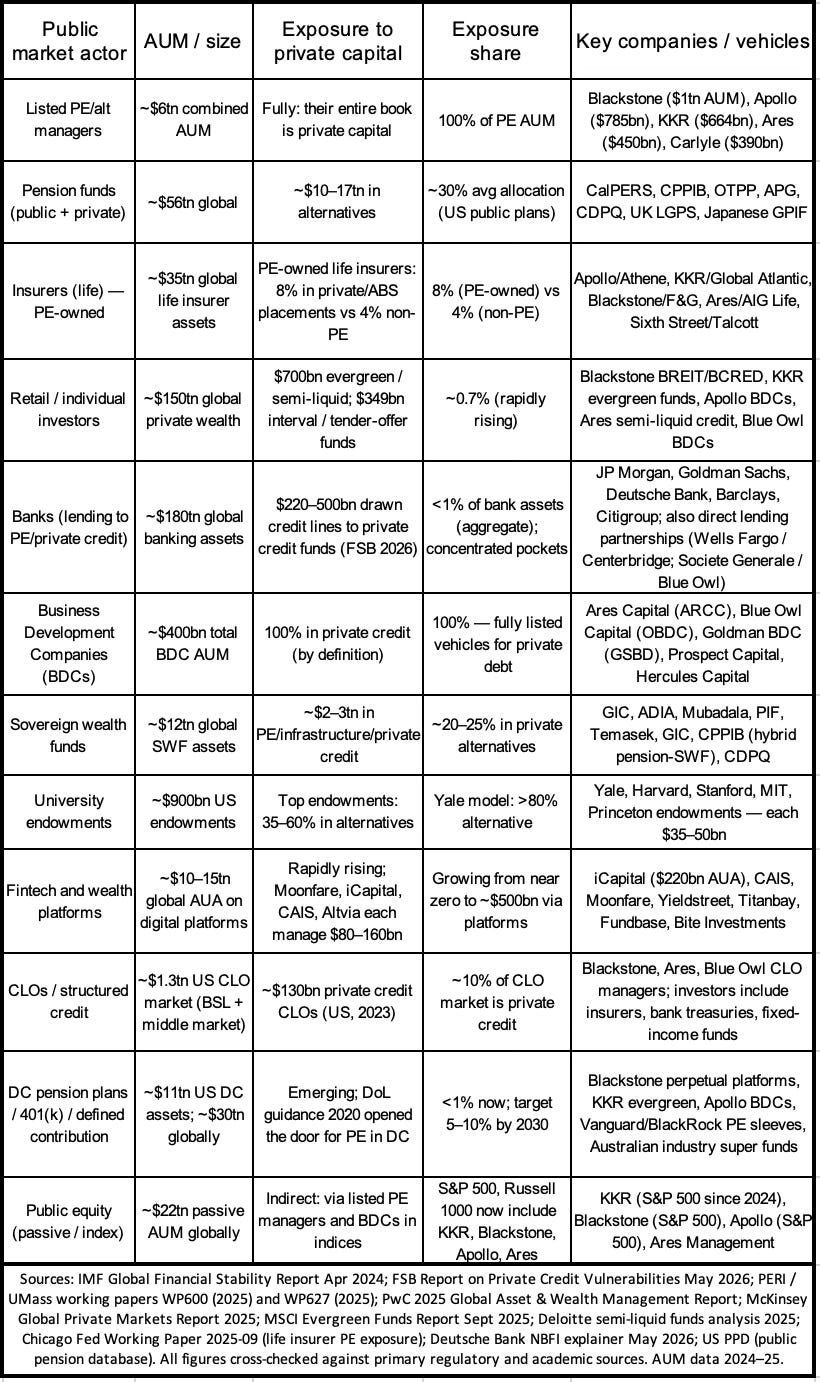

The table below is a summary of these investors and the extent of their exposures to private capital markets.

The sheer volume of private funds is staggering. Between 2020 and 2023, assets in private funds grew by 34%, from $20.8 trillion to nearly $28 trillion. This is only slightly less than the just under $31 trillion in assets held by public investment vehicles (mutual funds, ETFs, and closed-end funds). In 2024, 87% of companies with revenue greater than $100 million are private, and private funds have approximately tripled in size in the last decade to $26 trillion in gross assets, comparable to the $23 trillion US commercial banking industry. But their capital comes overwhelmingly from public institutions.

US public pension plans have allocated 34% of their holdings into alternative assets, including private equity, hedge funds, real estate, and commodities. The channel runs directly from workers’ retirement savings into PE buyouts of companies, hospitals, and infrastructure, with liquidity terms that have no resemblance to the pension’s own annual payout obligations. Similarly, the assets of private equity-influenced insurers have grown significantly in recent years, with these entities owning significantly more exposure to less-liquid investments than other insurers. By 2024, financial and ABS private placements reached 8% of assets for PE-owned insurers, while they were only 4% for non-PE-owned insurers. Apollo’s Athene, KKR’s Global Atlantic, and Blackstone’s insurance partnerships route annuity premiums, the most conservative class of retail savings, into direct lending.

The numbers alone make it abundantly clear that private capital cannot be a ring-fenced ecosystem of alternative assets with little public externalities. Private markets have become too big to be ring-fenced. Given the linkages discussed above, any stress in the private capital markets will immediately cascade across to public stakeholders and the markets as a whole.

It is now the hidden layer of the public financial system. Its debts appear in pension statements, its managers appear in index funds, its loans back annuities, and its performance propagates through bank balance sheets and university budgets. The “private” part is increasingly a regulatory and disclosure category, not an economic one.

There’s also the political economy that perpetuates the fiction around a ring-fenced private market. For one, private market intermediaries and investors benefit from favourable taxation regimes like carried interest and a lower capital gains taxation rate. There’s also the trend of diminishing public markets and expanding private markets, with its implications on access and equity, given the entry barriers for retail investors to access private markets.

Both these dynamics threaten to create two distinct financial systems, with one serving retail investors and the other serving those well-off. Worse still, while the latter can access the former and benefit from it without bearing the proportionate costs, the former must bear disproportionate costs and consequences of excesses arising from the activities of the latter.

The time has come to view private markets as no longer confined to sophisticated high-net-worth and institutional investors, but ones with deep interconnections with the public financial markets, and therefore demanding greater oversight and regulation. The matter for debate should only be the extent of regulation.

Unfortunately, such a regulation as a preemptive process is unlikely given the political economy dynamics. However, it is only one big crisis away from such regulation. This painful learning pathway may be unavoidable and the only route to private market regulation.

No comments:

Post a Comment