The pressure on the rupee in the aftermath of the Gulf War has generated considerable attention and discussion. I have blogged here on the implications of the Gulf War on India’s external account.

This may also be a good time to examine the dynamics driving the rupee downward. The rupee’s weakness is nothing new. Since the beginning of 2025, the rupee has been the weakest-performing EM currency, behind only the Turkish lira. As reported here, the rupee has weakened from 107 in early 2025 to 92 in the 40-country trade-weighted real effective exchange rate index, despite the RBI intervening heavily to backstop the decline. In fact, since October 2024, foreign investors have pulled out at least $45 billion, and their shareholding in Indian equities is currently at a 15-year low.

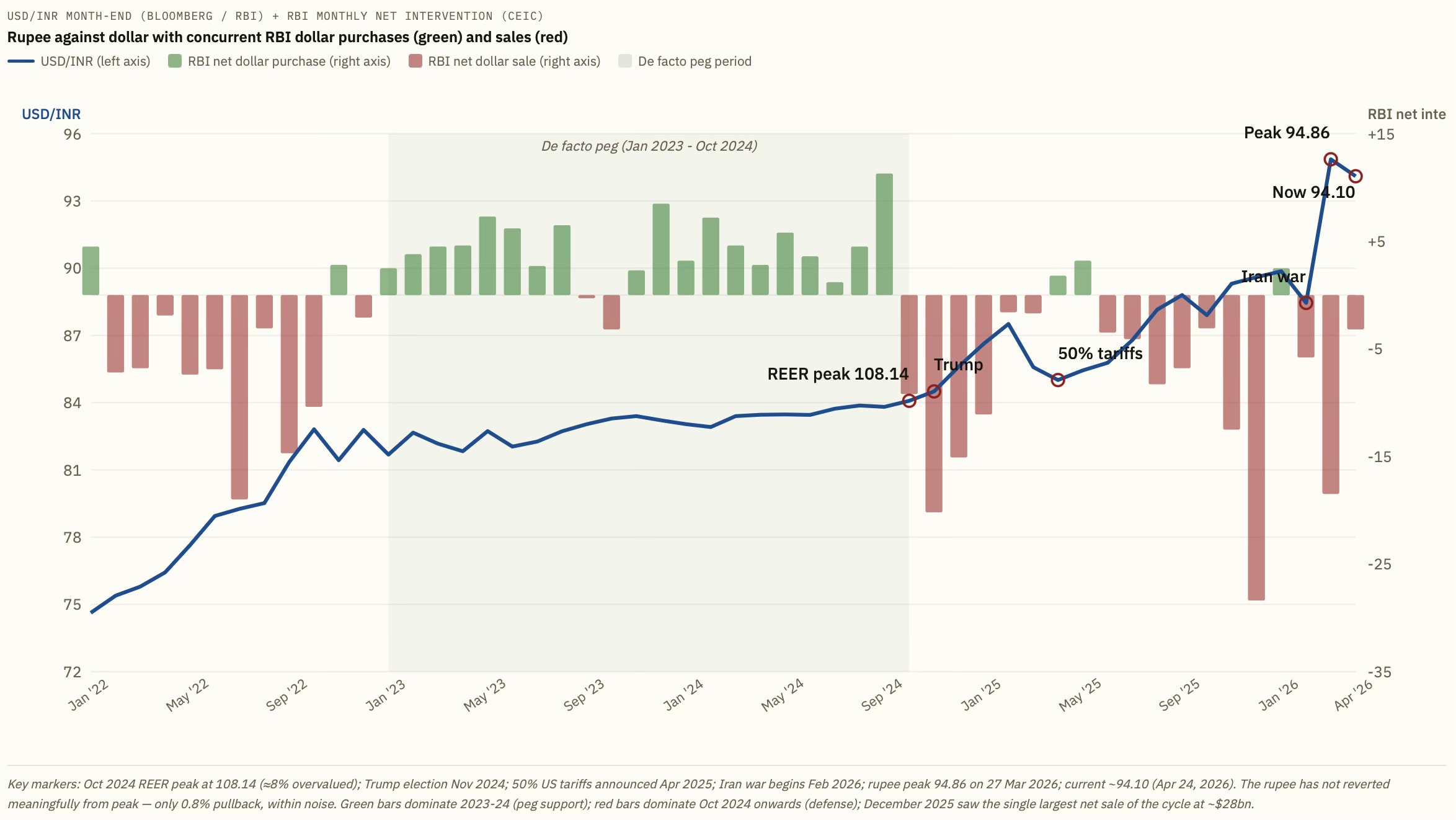

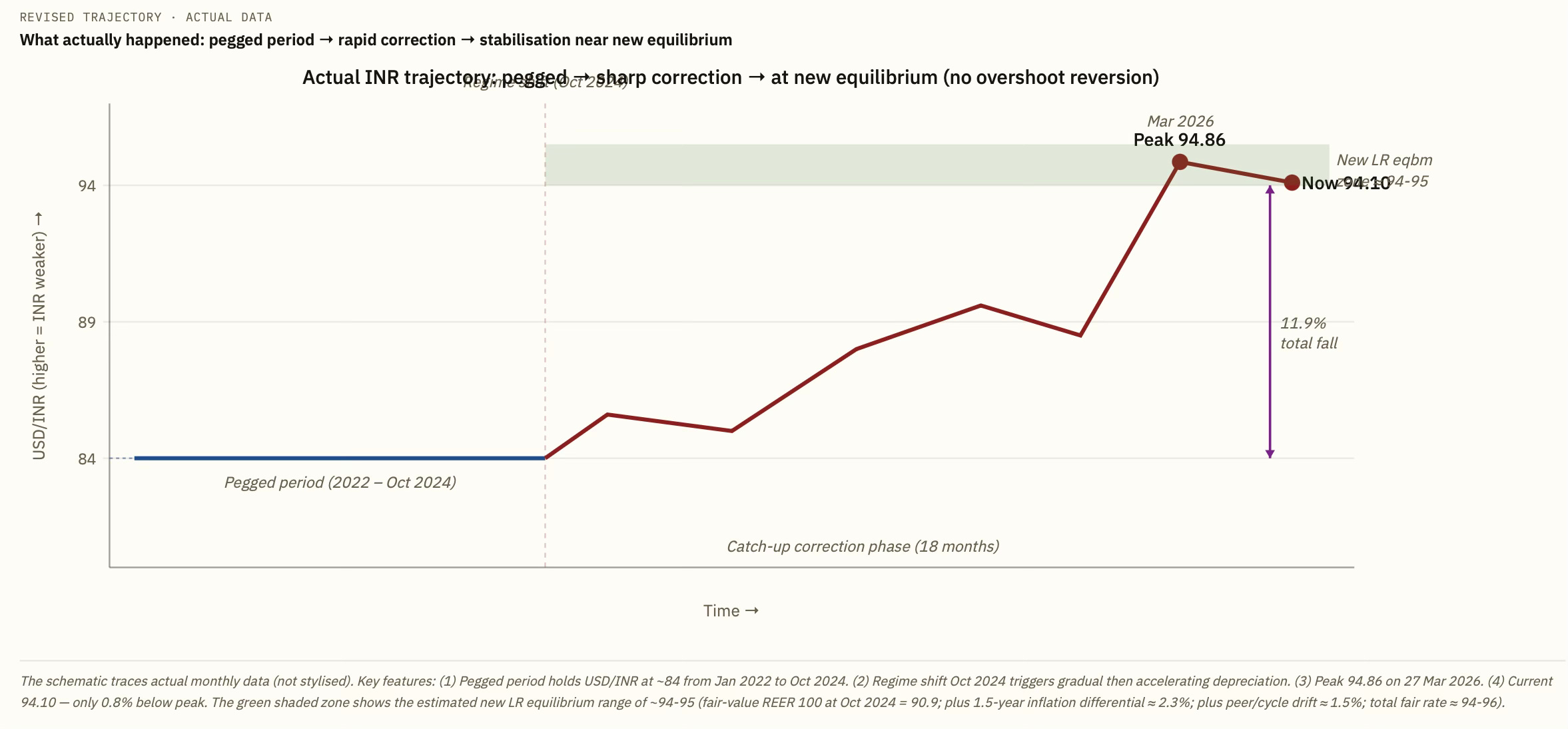

The graphic shows that the rupee held steady for two years, from at least the beginning of 2023 to the end of 2024, on the back of rupee purchases to prevent it from depreciating and find its level. In fact, compared to an annual USD-INR volatility of 5% in the 2000-22 period, the INR-USD volatility fell to just 1.8% during this period, the lowest in over 20 years, lower even than the 2000-2004 period when INR was effectively pegged!

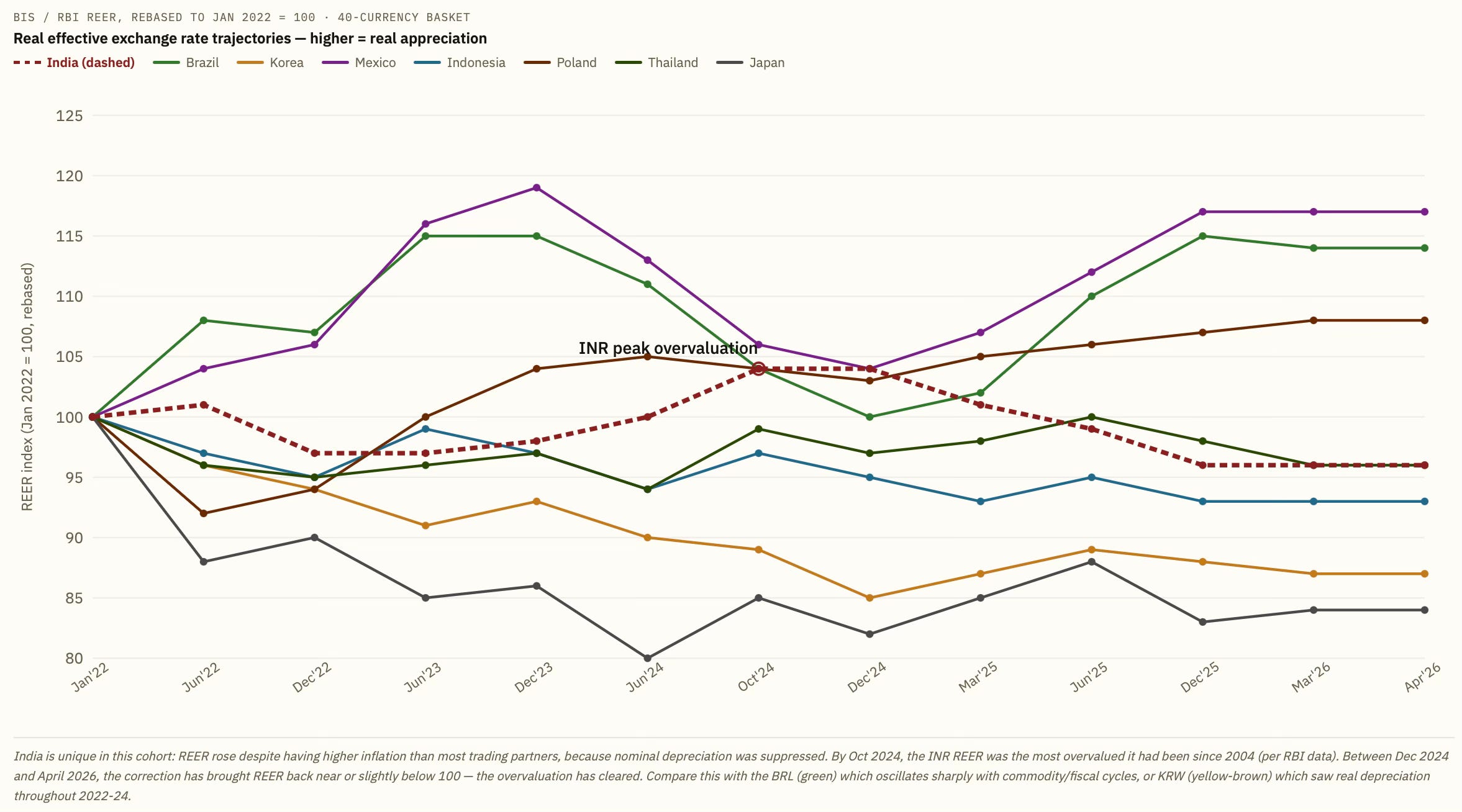

This drastic volatility suppression, combined with India’s higher inflation (CPI averaging ~5%) vs trading partners (2-3%), produced the biggest REER overvaluation build-up in the emerging-market universe during this cycle. The rupee’s 40-currency REER (base 2015-16) peaked at 108.14 in November 2024, and since then has depreciated sharply to below 95 by March 2026. This depreciation has been far in excess of any peer.

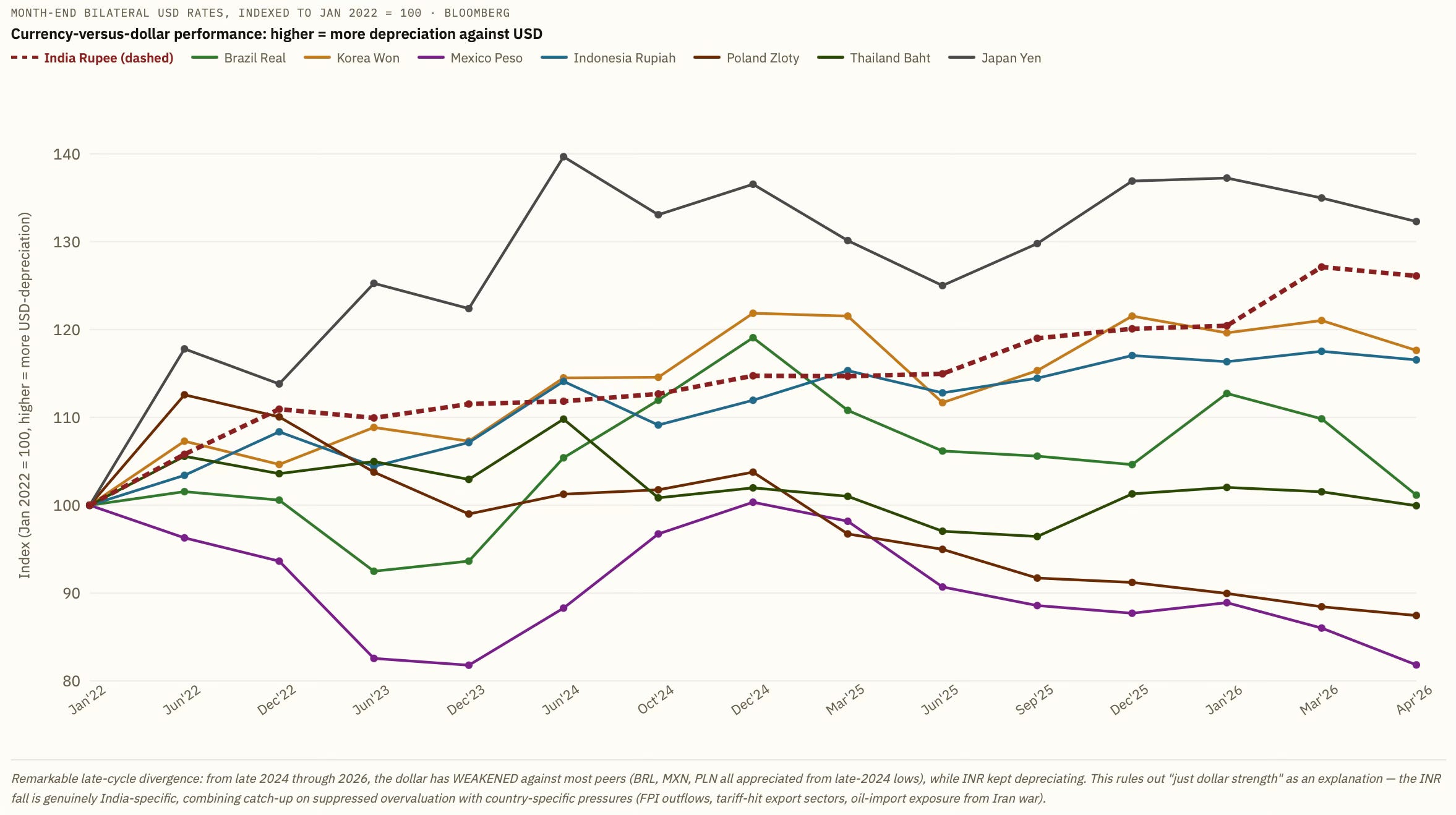

Similar trend is visible with respect to USD too. The rupee stands out for its unique flat trajectory through 2022-24 even as peers depreciated substantially in response to the Fed tightening cycle. However, since Oct 2024 the rupee has depreciated steeply, overtaking several peers.

It becomes clear that the rupee was held artificially overvalued for over two years. This, by itself, should have been reason enough that pressure mounted for a corrective depreciation. In addition, there was the pressure from the spike in oil prices (and associated worsening of the external account, already weakening from the tariffs and FPI repatriation) and the general trend of risk-off and capital flight to the safety and liquidity of the dollar.

By itself, the Gulf War would have put enough pressure on the currency. But its combination with the stress built up due to the forced overvaluation amplified the capital flight induced by the Gulf War, thereby exacerbating the pressure on the rupee and worsening the depreciation when it happened.

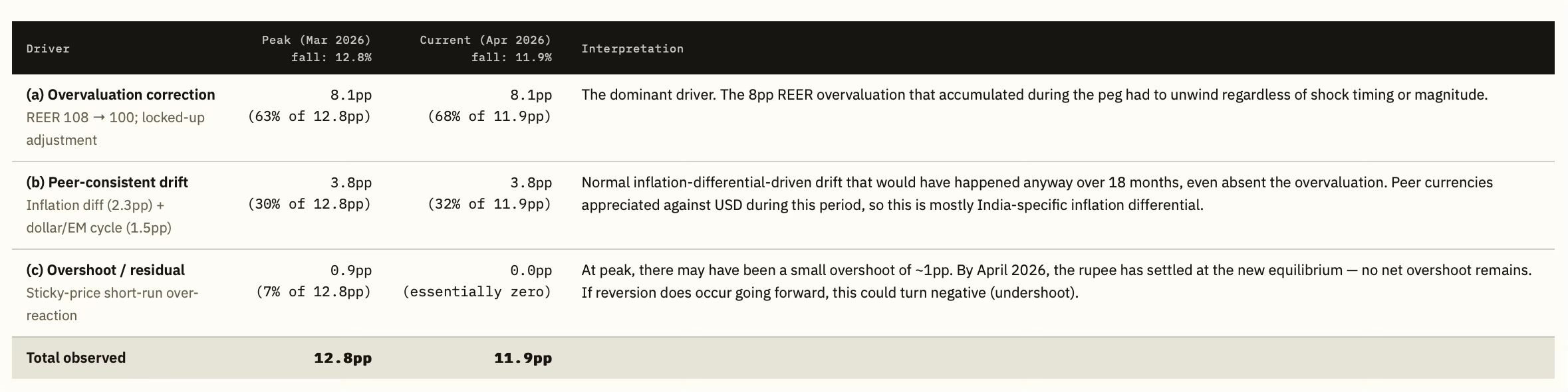

The table below is a quantified decomposition of what drove the 11.9% depreciation. It shows two alternative decompositions at the peak (Mar 2026), which capture the overshoot moment, and at current levels (Apr 2026), after partial reversion.

At peak (Mar 2026), the biggest driver by far was the overvaluation correction (63% of the fall), which is the “hidden cliff” the RBI’s peg concealed and which was unique to the rupee. The general market volatility (36%), experienced by all peers, was a secondary driver, reflecting genuine dollar/EM repricing. The net overshoot, at least till now, has been negligible.

Has there been a Dornbush overshoot? Rudiger Dornbusch's 1976 overshooting model predicts that when exchange rates are flexible, but goods prices are sticky, a monetary or policy shock causes the exchange rate to overshoot its long-run equilibrium before reverting. In simple terms, if the currency has been artificially propped up, the "stickiness" is extreme, and therefore, when the adjustment finally comes, the overshoot magnitude is larger than in a regime of continuous flexibility. However, the Dornbusch overshoot and reversion are not yet visible. The reversion might happen in the coming weeks.

So what are the lessons?

By maintaining the rupee as a de facto pegged currency from 2023 to October 2024, the RBI accumulated an 8% REER overvaluation that had to be corrected. When the regime shifted — Trump election, FPI outflows, US tariffs, Iran war — the correction was both deeper and faster than peers experienced, precisely because the catch-up component (8pp) was additive to normal drift (3.8pp). The rupee is now at or near its new equilibrium of ~94-95, down 11.9% from Oct 2024.

The RBI’s 2022-24 intervention pattern - buying ~$400bn in forex reserves while keeping the rupee rigid - converted exchange-rate risk into reserve-allocation risk. When the regime shifted, reserves fell by $80bn in four months without preventing the correction. Further, the sharp Mar 2026 overshoot caused imported inflation, margin stress on exporters who had hedged at 84, and a sudden repricing of corporate foreign-currency debt. A gradual depreciation path through 2023-24 (releasing 3% per year against the peer-consistent rate) would have spread this adjustment at much lower systemic cost. The rupee has done exactly what a freely-floating currency would have done gradually over 3 years, but compressed into 18 months because the peg delayed adjustment, and with serious credibility cost (for investors).

The speed of adjustment was consistent with Dornbusch dynamics (7.2% in a single month from Feb to Mar 2026 is unprecedented for INR). However, the second half of the Dornbusch pattern - reversion toward long-run equilibrium - has not so far materialised, though it could yet in the coming weeks. The rupee is currently 94.10, only 0.8% below its 94.86 peak. This is within noise, not meaningful reversion.

This is a teachable moment on currency management for central banks. Policies that keep a currency overvalued are always counter-productive, especially for developing countries that are always at risk of being caught in an episode of sudden stop and capital flight. When such episodes are triggered, the overvalued currency invariably experiences a steeper slide and greater overshoot, with all attendant consequences. Most importantly, steep devaluations convey a macroeconomic instability signal to investors. It increases the country risk for investors, who must now factor in the likelihood of episodes of sharp depreciation risks while making their investments. It is a dent in the central bank’s credibility.

The rupee is going through one such episode. The original sin may have been committed in the 2023-24 period.

No comments:

Post a Comment