The shock in the UK market for liability driven instruments (LDI) has drawn attention to the issue of hedging for gaps in the existing defined benefit (DB) pension schemes, and the larger issue of returns for pension funds. Along side the declining returns on investments, at least for sometime, pension funds (DB ones) face the problem of rising inflation and therefore higher inflation adjusted pension liabilities.

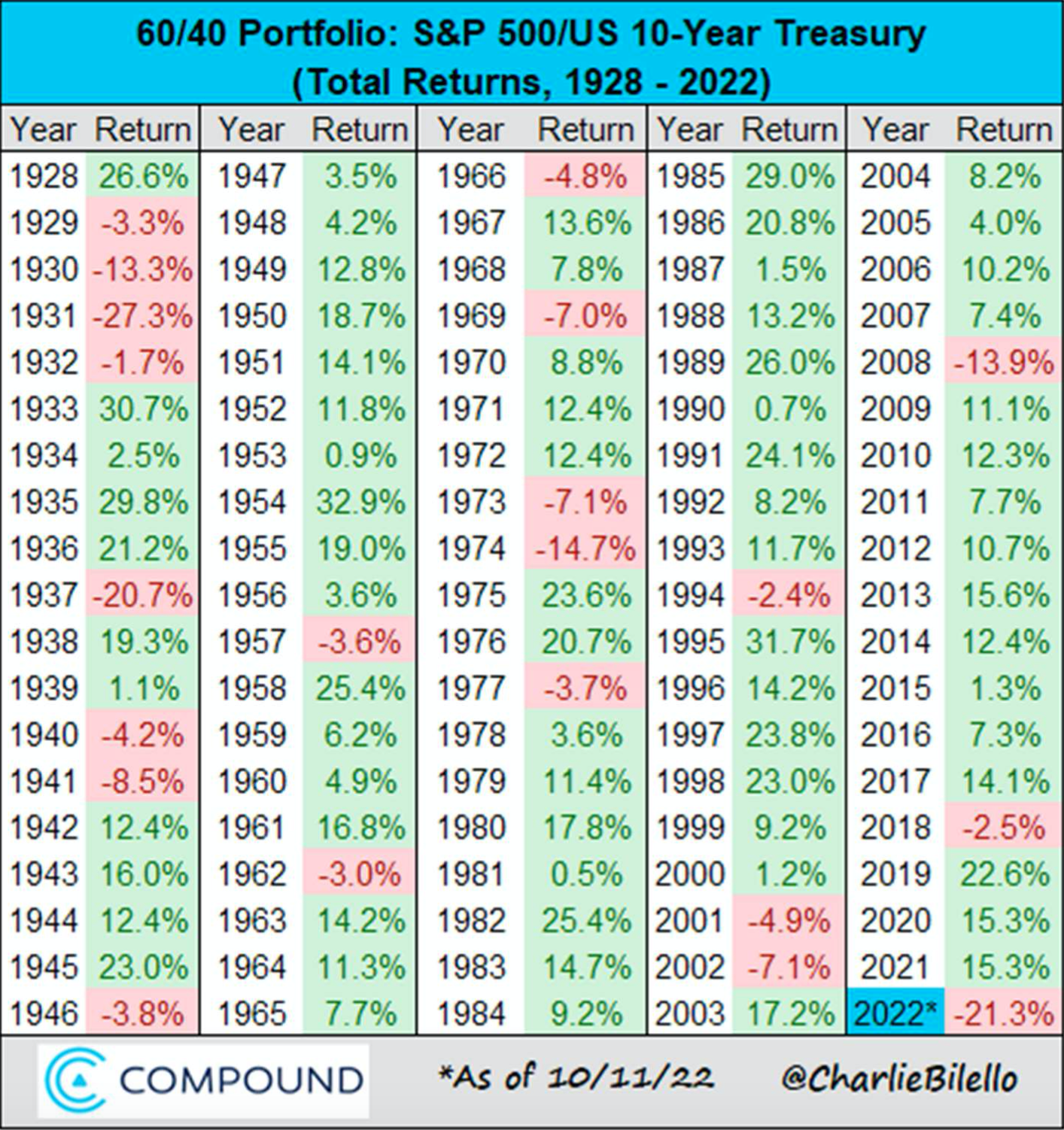

John Mauldin points to how the traditional 60:40 stocks to debt portfolio, the workhorse portfolio of investment, is being whacked this year, as bonds are having one of their worst years ever.

Years of falling interest rates raised pension liabilities—a big problem for plan sponsors and managers. Lower interest rates reduced the return on the bond portion of a pension fund. In a world of zero and negative interest rates, pension funds simply couldn’t make their target returns (typically 7% and sometimes more) when 40%+ of the portfolio was making 2‒3% (at best!). Consultants then pushed them toward something called “Liability-Driven Investment” or LDI, basically a leveraged hedge fund strategy betting interest rates would keep dropping. They showed data that for the last 30 years the trade ALWAYS won. Except the last 30 years was a period of falling rates and inflation, which everyone assumed would continue. It worked well until rates went higher.

In the US, the problem is not with LDIs but the high exposure to equities and alternative assets, which could have an extended period of downturn.

Asset allocation by the UK’s 5200 odd DB schemes has shifted dramatically over the past 15 years. These funds collectively have more than 10mn members and £1.5tn assets under management. At the end of 2021, they were 72 per cent allocated to bonds, 19 per cent to equities and the rest to other investments such as property and hedge funds, according to the Pension Protection Fund, the lifeboat scheme for the sector. This contrasts with 2006, when they were 62 per cent invested in equities and 28 per cent in bonds. This trend reflects how regulation and politics have pushed DB pension funds out of equities to invest more heavily in bonds, which are considered “safe” assets that reduce the risk to the portfolio and sponsoring employer.

On the issue of pension systems, Mauldin points to a Mercer report that evaluates different pension systems.

Economic sandpiles that have many small avalanches never have large fingers of instability and massive avalanches. The more small, economically unpleasant events you allow, the fewer large and, eventually, massive fingers of instability will build up.Efforts by regulators and central bankers to prevent small losses actually create the large fingers of instability that bring down whole systems and spark global recessions. And, increasingly, the unfunded liability of government promises will be the most massively unstable finger.In that crisis, things that should be totally unrelated will suddenly become intertwined. The correlations of formerly unrelated asset classes will all go to one at the absolute worst time. Panic and losses will follow. Governments will try to stem the tide, perhaps appropriately so, but, eventually, the markets have to clear.There is a surprising but critically powerful thought in that computer model from 35 years ago: We cannot accurately predict when the avalanche will happen. You can miss out on all sorts of opportunities because you see lots of fingers of instability and ignore the base of stability. And then you can lose it all at once because you ignored the fingers of instability.

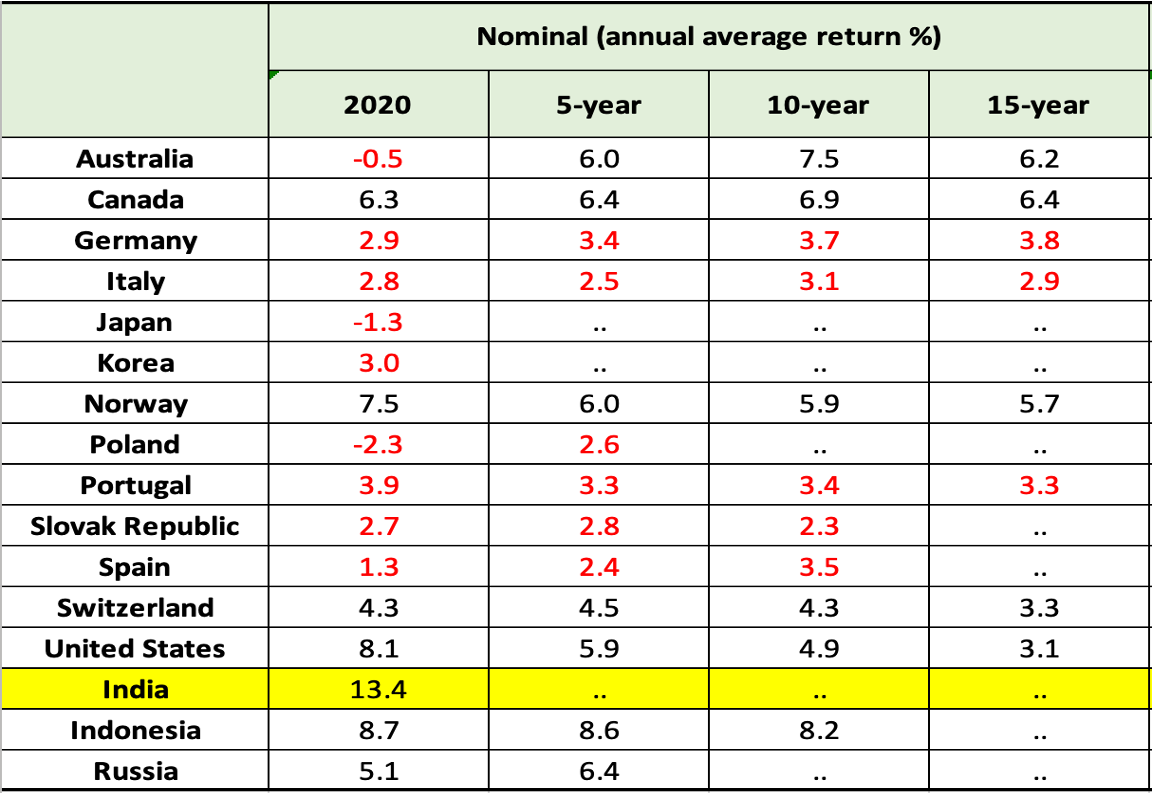

The point about the risks with DB plans is of relevance to India too. The high returns earned by the New Pension Scheme (NPS) trust till date should not blind us to the strong likelihood (I would go so far as to say near inevitability) of far lower returns in the decades ahead. As the OECD Pensions Survey indicate, India's annual average returns are much higher than in any other country.

This is perhaps validated by the much higher 10 year government bond yields in India compared to the standards of emerging economies, a trend which cannot be sustained as the country undergoes more global financial market integration.

I had blogged earlier drawing attention to the role of demographics and other factors in contributing to a secular decline in global interest rates. There is nothing to suggest that the same should not apply to India. Taking all together, the days of near double-digit pension growth rates clearly appear on the rear-view mirror.

All this makes the trend on reversion to defined benefit pension schemes in some Indian states even more disturbing.

No comments:

Post a Comment