The formal adoption of China’s 15th Five-Year Plan has generated much scrutiny and analysis.

The central theme is the development of a modernised industrial system, elevating it above the regular headline of technological innovation. The sequencing reflects a practical focus: turning laboratory breakthroughs into scalable, high-value production capacity. Frontier sectors such as advanced manufacturing, semiconductors, next-generation information technology and aerospace are prioritised. The plan aims to achieve breakthroughs in critical areas, including semiconductors, industrial machinery, advanced materials, biotechnology, and foundational software, and to deepen integration between scientific and industrial innovation.

Importantly, it does start to acknowledge the role of the structural imbalances in the economy. For example, under the overarching banner of “common prosperity”, it links household-centred policies to growth resilience: employment, childcare, education and social safety nets are no longer simply "livelihood" issues — they are productivity and confidence issues. But this focus on structural empowerment appears, as I discuss later, to be done in a more roundabout manner.

The Plan has some clear departures from earlier versions, prompted by internal and external challenges. As mentioned, the elevation of the industrial system before innovation indicates a shift from the lab to the factory floor. Related is the focus from making breakthroughs to applying them at scale. It offers an opening up of high-technology sectors and deepening cooperation in specific regions and industries.

In short, the 15th Five-Year Plan appears to mark a subtle shift from scaling up to sharpening China's edge — a strategy designed for a world of intensifying great-power competition, supply chain fragmentation, and technological rivalry. Its effects will be felt well beyond China's borders, influencing global trade flows, technology standards, and the competitive landscape across nearly every advanced industry.

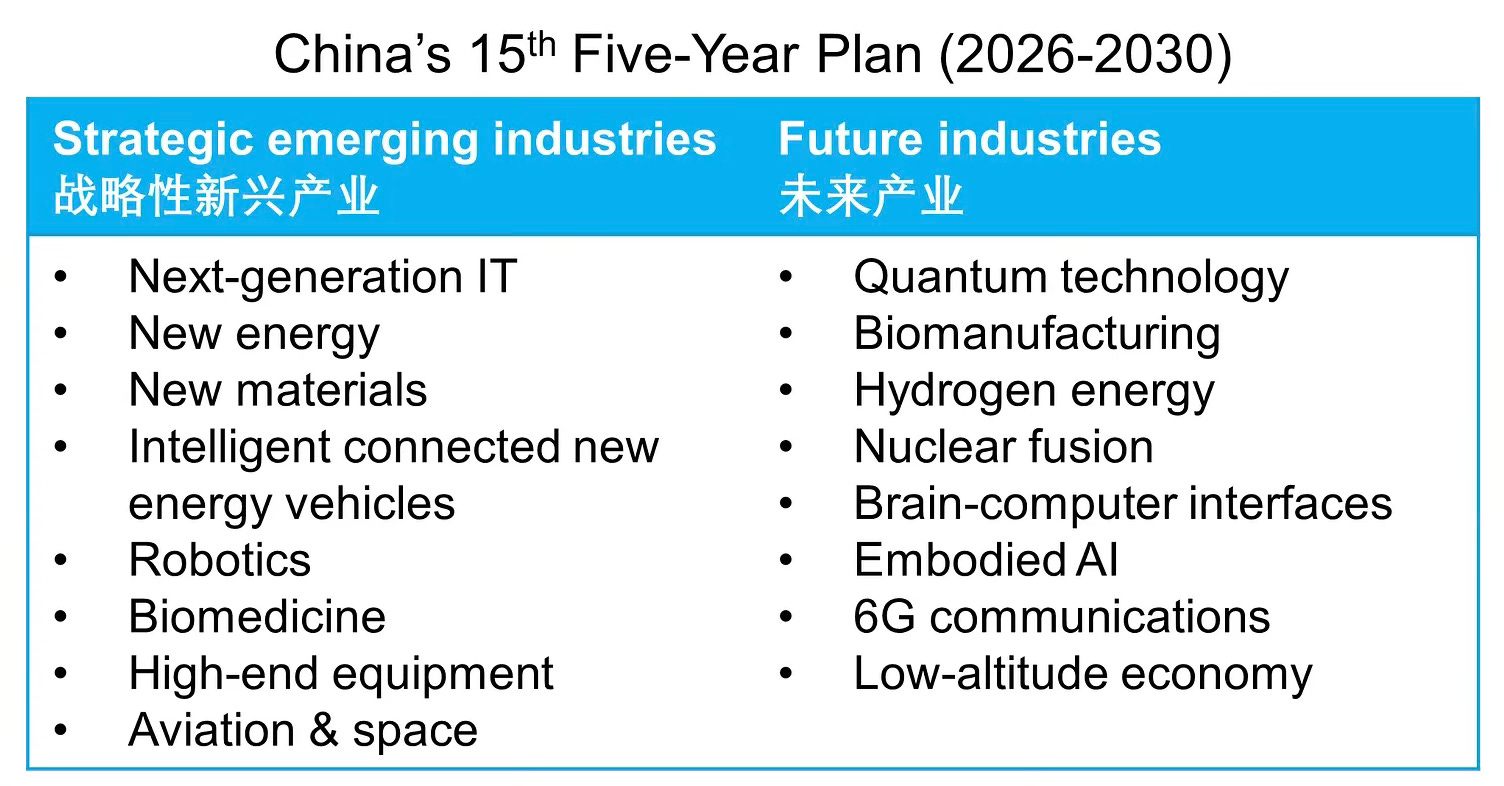

Kyle Chan has an excellent analysis of the technology and innovation focus of the Plan. It focuses on strategic emerging industries and future industries as “new quality productive forces” to achieve the income level of a moderately developed country by 2035 (or socialist modernisation).

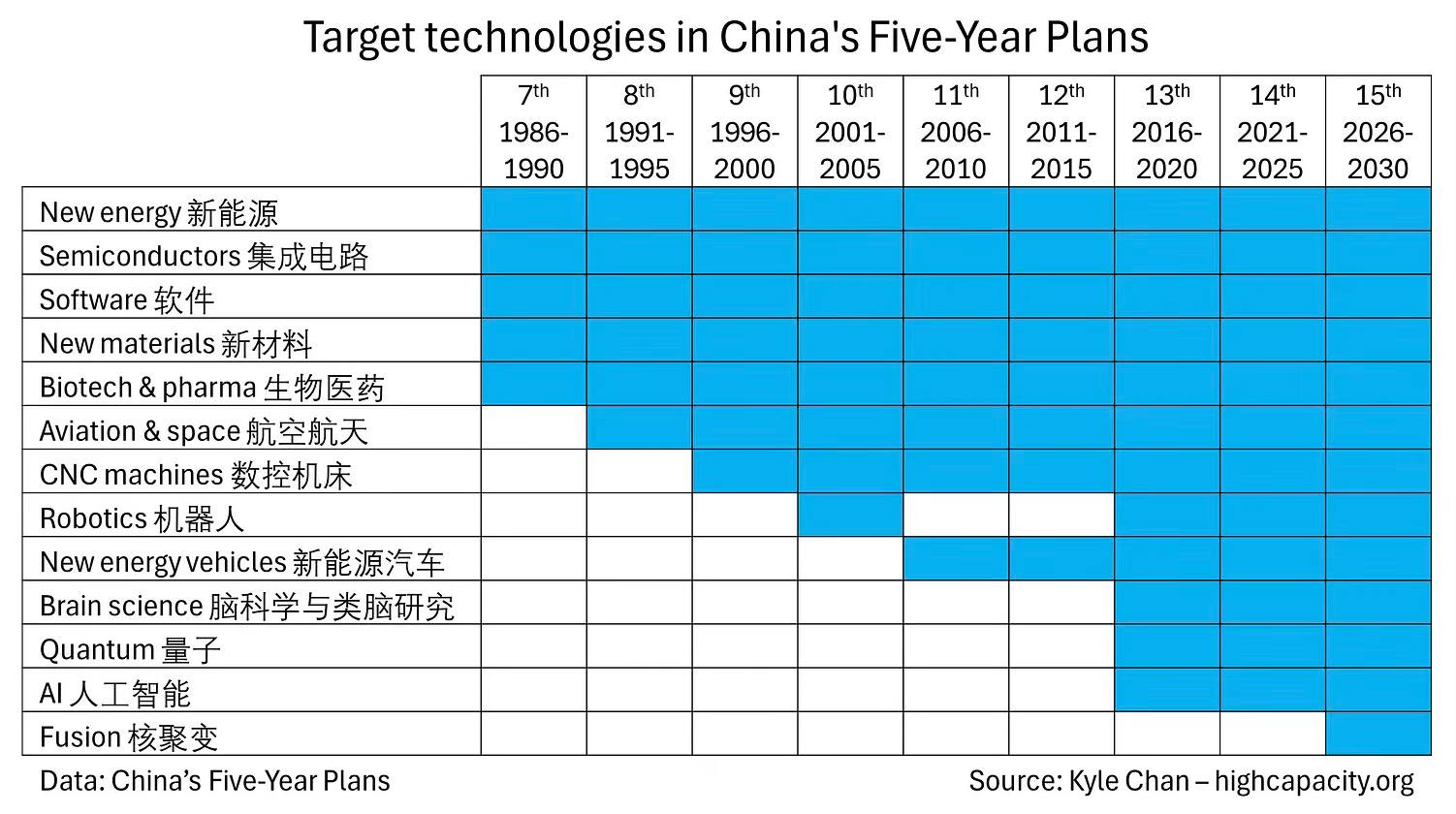

A less discussed feature of China’s economic success is the long-term planning and persistent pursuit of the plan objectives.

What makes China’s tech-industrial policy remarkable is not some hundred-year master plan for technological supremacy or meticulously engineered blueprint for success. It’s China’s sustained focus on a set of obviously critical technologies over years and even decades. While the strategies and tactics—and even the technologies themselves—may change, China’s overarching persistence has yielded steady gains that have allowed it to catch up and even achieve global leadership in key technologies. China’s new 15th Five-Year Plan is but the latest chapter in a much longer technology story.

The Five-Year Plans have shifted from top-down guidance to a broader strategic guidance framework.

The aim of the earlier Plans was rapid industrialisation and catch-up with a focus on heavy industry… Today’s Five-Year Plans serve as strategic roadmaps for China’s development and include a mix of qualitative goals and hard quantitative targets. Each part of the Five-Year Plan is broken down by sector and annually. Central government bodies and local governments then break down the Five-Year Plan and develop their own implementation plans. Local government officials are evaluated in part on their performance in meeting the national plan’s goals and targets. In general, China’s Five-Year Plans are best understood today not as rigid, top-down “plans,” but as high-level signaling mechanisms that guide local governments and the private sector to align their efforts with national priorities.

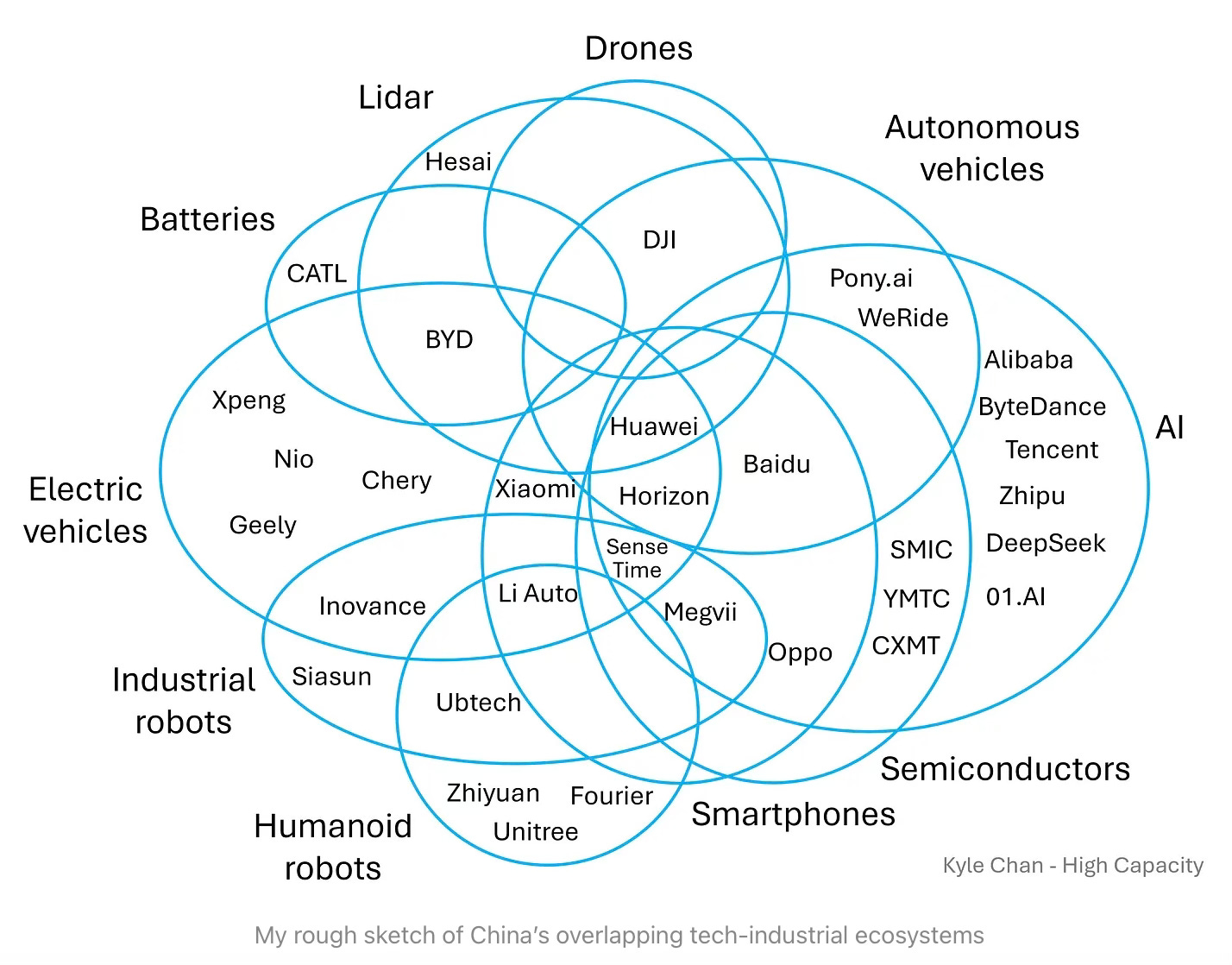

In this context, in an earlier post, Kyle Chan had pointed to China’s industrial policy strategy of creating interlocking industrial ecosystems that allow it to play across the manufacturing spectrum.

China doesn’t just have a smartphone industry or a battery industry or an electric vehicle industry. It has all of these industries and more. China’s strength across multiple overlapping industries creates a compounding effect for its industrial policy efforts… If you’re trying to develop a target industry, it helps to have the technology and manufacturing capacity in surrounding industrial domains… industrial policy is like a jigsaw puzzle. The more pieces you already have in terms of technology and domestic manufacturing capacity, the closer you are to filling in the remaining gaps. And if you’re already strong in multiple overlapping industries, then this creates a mutually reinforcing feedback loop that further strengthens your position in all of these connected industries… As China becomes stronger in some industries, this tightens its grip on others…

Having existing domestic suppliers in upstream industries can make it easier to source parts and work directly with suppliers to modify specifications to suit industry needs… Having an existing set of domestic buyers in downstream industries can provide a ready source of market demand and industry revenue… Technical knowledge and manufacturing know-how can be useful across industries. Investments in R&D and manufacturing techniques in one industry can have returns across other related industries… If you have a product that’s an input for multiple industries, then having all of those industries domestically allows for greater economies of scale for that product.

Another notable insight from the Plan is its focus on higher-quality cultural and consumer goods as a national priority. Innovation extends as a cross-cutting policy mandate, underpinning everything from public welfare and soft power to trade and defence. The Plan talks about boosting “cultural confidence”, whereby Chinese citizens (and the world) feel pride in, and aspiration toward, Chinese-made goods and cultural products, not just Western ones. It refers to building a “cute, respectable image of China” through overseas Chinese film festivals, museum upgrades, high-quality art and literature, video games, animation, exhibitions, cultural tourism, and new public cultural spaces. It also includes the phrase “enable the people to enjoy a higher quality cultural life.”

The Plan’s emphasis on stimulating domestic demand offers longer-term opportunities in sectors tied to lifestyle upgrades- dine-in consumption, fitness, outdoor sports, live entertainment, cultural activities, gaming, and digital content, and high-end dining, boutique travel, wellness services, and premium lifestyle experiences. This is a definitive signal that China has now openly embraced the lifestyle of capitalism.

Carolyn Marie Yim has a good post that draws attention to the idea of Cool China as one where the country is increasingly producing things people want to buy, emulate, and follow, much as Japan made a similar transition from "cheap copy" to global design leader in the 1970s–80s. She writes,

This does not mean every Chinese consumer product will win, or that the world will wake up one morning and consciously decide to prefer Chinese made goods. Historical transitions are less theatrical than that. More likely, Chinese-made and designed goods will become globally normal the way post-war Japanese and German products normalized from cheap into high quality signifiers of quality and manufacturing. Moreover, consumers will not necessarily experience this as geopolitical preference. They will experience it as the increasingly common sensation that the nice plate, the good lamp, the respectable glasses, the favorite sweater, the pleasant cafe, the fun Chengdu trip, all seem to come from the same logistical and economic base.

This focus on cultural capital is, I suspect, coming from an interest in the promotion of soft power and is less about addressing the structural imbalances. The resultant policies, for sure, will have some impact on the consumption side and might even be interpreted as a focus on addressing the structural imbalances. I’m not sure.

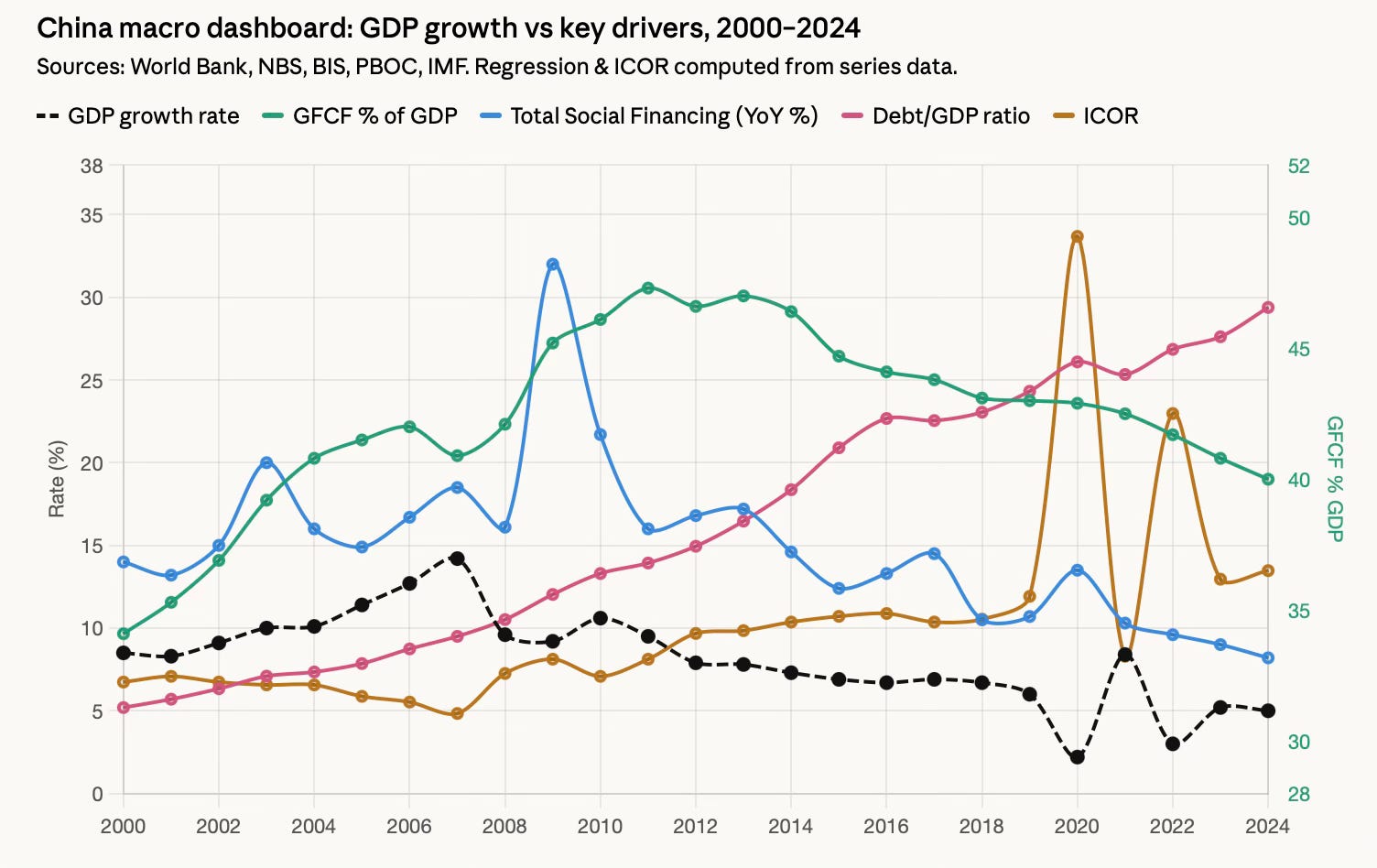

The 15th Plan comes at a time when the economy is slowing, and the limits to the input-based model are becoming evident. Credit-fuelled investment has been the primary driver of economic growth.

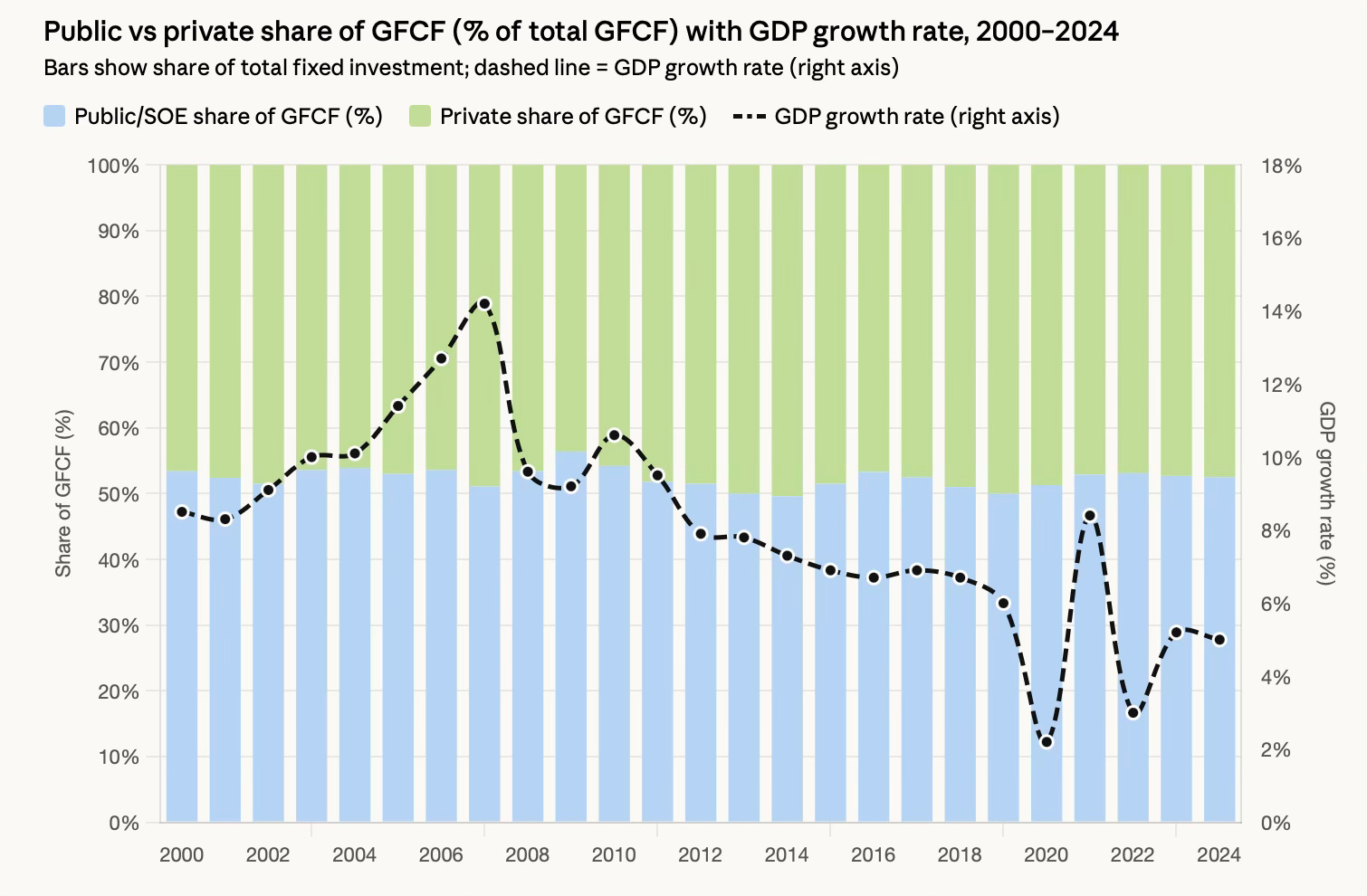

Remarkably, all through the quarter century, even as the private sector has emerged as a major partner in economic growth, public spending has remained elevated at more than half of the output, and has hardly budged from 53.4% of the total GFCF to 52.5%.

Raising questions about the quality of public spending, since 2010, the Incremental Capital Output Ratio (ICOR), a measure of investment quality, has steadily risen and nearly doubled since 2010 to 7.6 in 2024. It appears that, economy-wide, the efficiency of China’s investment quality has declined alarmingly.

This backdrop is important insofar as it offers valuable lessons. The central failing of China’s economic growth model has been its perpetuation of a structural imbalance between consumption and investment. In the first phase, it was about loading investments into physical infrastructure, including housing and the development of greenfield townships. The excess capacity built up on the infrastructure supply-side was sought to be exported globally through the Belt and Road Initiative (BRI).

Since 2015, the 13th Plan period has seen an increase in industrial focus and investments. This got amplified following the 2021 bursting of the housing bubble, with the government going into overdrive on manufacturing capacity expansion, with a focus on frontier technology areas. It also spawned massive increases in investments in R&D and innovation in areas like green technologies, electro-tech, semiconductor chips, and AI. Again, borrowing the playbook from BRI, the excess capacity was exported globally, resulting in the country’s trade surplus hitting $1.2 trillion in 2025.

In both these phases, the domestic structural imbalances were sought to be papered over by focusing on building capacity and exporting the production globally. It was like China decided to make infrastructure and industrial capacity at home for the world. Never mind whether the world wanted it that way or not.

Now, as growth flags and as structural imbalances continue to persist, the 15th Plan has proposed that the “new quality productive forces” emerging from strategic emerging industries and future industries can be the driver of growth to realise an income level of a moderately developed country by 2035. An important political (and economic) signal is that the Plan aims to maintain growth between 4.5-5% for 2026, a compulsion that is an important factor driving the growth strategies pursued. In simple terms, it is about shifting focus to the development of advanced industrial ecosystems in frontier technology areas. It has the added imperative and justification of the new Cold War with the US and the West.

If we go by the track record, the assumption among Beijing’s policy makers is that it would lead to another Plan period of more or less similar inputs-based industrial growth (albeit in frontier technology areas), fuelled both by domestic demand and global markets.

I’m not sure whether these assumptions will hold. This time may well be different. As I blogged here, there are now emerging hard limits to the inputs-driven growth model. Further, as geopolitical tensions rise and the Cold War deepens, China’s access to advanced technologies and equipment will become scarce, forcing Beijing to pour more resources into developing the same internally. Given the technologies involved, the nature of the resource allocation challenge, especially to do so efficiently and effectively, is much bigger and more complex than throwing resources into developing infrastructure and industrial capabilities. I’m not sure that pouring resources into large public and private companies, even with the most militantly patriotic and idealistic motives, can help create the conditions to deepen links between innovation and the manufacturing industry and foster the deployment of frontier technologies.

This would be like one country trying to mobilise all the resources to compete with the world at large in developing its own proprietary frontier technologies. The Soviet example, which did not end too well, notwithstanding very important differences, is not to be ignored.

The external market access, even in developing countries, is facing strong pushback or is rapidly closing. No large middle-income developing country, those with the markets to meaningfully absorb the Chinese excess capacities, will countenance a flood of cheap imports that will not only make them acutely dependent on another country in strategically important sectors, but also weaken and destroy their own domestic industrial capabilities. The rising backlash from the world economy’s China problem is another salient limiting factor to the pursuit of export-based economic growth strategies.