1.

Fascinating illustration of perception of probabilities,

2. Nice

overview of the Unified Payment Interface (UPI) inter-operable immediate digital payment system that has been launched in India.

3. The

FT captures the irony of Trump's misguided embrace of Saudi Arabia and ostracism of Iran as a battle between "good and evil",

While Mr Trump unleashed a storm of anti-Iran rhetoric, millions of Iranians danced and sang in cities across the country celebrating Mr Rouhani’s victory — scenes that would have been anathema to Saudi Arabia and other Gulf monarchies. The crowds lauded the 2015 nuclear deal, while gushing about the potential for reform and their desires for Iran to engage with the outside world.

What he instead tore up in Riyadh was any attempt to pursue what Mr Obama hoped would flow from the deal: regional detente between Sunni and Shia in which their regional champions, in Riyadh and Tehran, “share the neighbourhood”

The emphatic victory of Hassan Rouhani over hardliners is a great opportunity to bring Iran on to the fold. But that is something which neither Israel nor Saudi Arabia would want. And Trump is playing into their hands.

5. In the context of China's ratings downgrade,

Times captures the staggering scale of China's credit expansion and debt accumulation,

When it comes to pumping money into a financial system, China has made the Federal Reserve in the United States and the European Central Bank look almost lackadaisical. It has expanded its broadly measured money supply by more than the rest of the world combined since the global financial crisis. Now it has 70 percent more money sloshing around its economy than the United States does, even though the American economy is bigger. China has accumulated its towering debt remarkably quickly. Goldman Sachs looked last year at how fast debt had accumulated relative to the size of the economy in 55 countries since 1960. It found that by the end of 2015, China was already in the top 2 percent of all credit expansions — and its debt shot up even higher last year. All of the other large expansions occurred in very small economies, some of which essentially lost control of their finances.

And all this is excluding the shadow banking system as well as the off-balance sheet wealth management products of banks. Incidentally this is China's

first ratings downgrade since 1989!

6. Predictably the Chinese officials have lashed out at the rating agencies. But, here the Indian government may have a much more compelling reason for nursing a grudge against them. Ananth points to

this very good article and the graphic is pretty much self-explanatory,

Consider this,

The GDPs of Italy and Spain are projected to grow at much lower rates than India’s and Indonesia’s. The level of government, corporate and household indebtedness is significantly higher than India’s and Indonesia’s. Italy and Spain share India’s problem of a high level of bank non-performing loans (NPLs). The one metric in which the two countries outperform India and Indonesia is GDP per capita. Yet Fitch and S&P rate Spain two notches higher than India and Indonesia, while Moody’s has assigned a rating that is one notch higher. Further, S&P has assigned a positive outlook on Spain’s rating but a stable outlook on India’s rating. Similarly, Fitch and Moody’s have assigned ratings to Italy that are a notch higher than India’s sovereign rating, while S&P rates India and Italy on a par. This is despite Italy’s ratio of bank NPLs to total gross loans being more than twice India’s NPL ratio!

And the reason is the bucketing methodology that rating agencies follow,

The impediment to the rating agencies upgrading India’s sovereign ratings lies in their methodologies. The sovereign rating methodology factors economic strength, institutional strength, fiscal performance, and susceptibility to event risk to assign ratings. The rating agencies categorise countries into buckets based on their size (GDP), growth, volatility of growth and per capita income, among other factors. The emphasis on per capita income is because countries with higher per capita incomes are better equipped to withstand cyclical volatility and are endowed with higher debt servicing ability. India’s low per capita income has resulted in its sovereign rating being lower than countries with higher deficits and indebtedness and lower growth prospects.

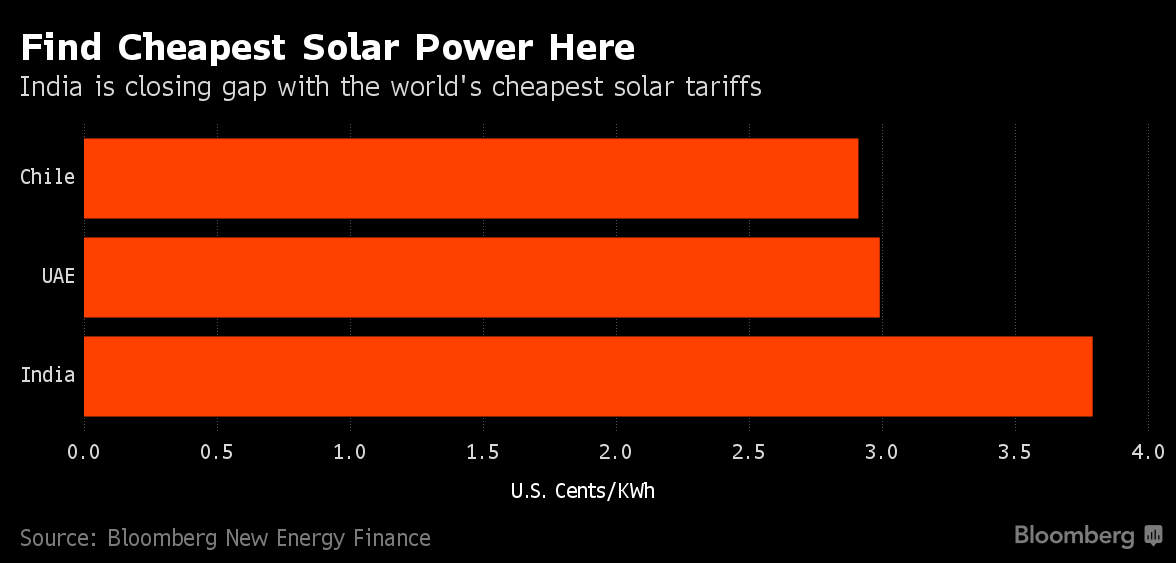

7. A

perspective on how much renewables are transforming global electricity markets,

Today, renewables account for an average 23 per cent of global power output. Denmark has breezy days when all its power comes from wind and Germany hit a record 85 per cent share from renewables one day last month.

8.

Adam Gopnik draws an interesting conclusion from the contrasting responses of the conservative establishments in the US and France during their respective recent elections,

In France, as in America, the election pitted an extreme right-wing nationalist against a moderate technocratic liberal, but in France the leaders of the “Republican” right recognized the extreme nationalist right as a threat to democratic values and, after one round of voting, supported Macron, a man of the center-left who had served in a Socialist government. In this country, the leaders of the Republican Party made the opposite choice.

That difference made all the difference. The space between François Fillon, the defeated right-wing candidate, and Macron is, in ideological terms, every bit as large as the space between, say, Marco Rubio and Hillary Clinton. But Fillon understood that a Marine Le Pen in power would be a threat to the nation’s constitutional structure. The irony was that the French, with their (mostly unearned) reputation for craven surrender and opportunism, held fast to their deepest principles, while mainstream American rightists discarded theirs.

9. India's job market is

ringing alarm bells, loud and clear, with even the much vaunted IT sector jobs hiring on the decline,

The overall index for April 2017 was 10.9% lower than a year ago. That means new job creation in the month was 10.9% lower than April 2016. What’s more, the overall index for April 2017 was lower than where it was in July 2015. Compared to April 2015, the index is up a mere 1.8%, indicating the glacial pace of job creation. Among sectors, the worst hit was the information technology (IT)-software industry, which saw a 24% year-on-year drop in hiring. Apart from stricter employment norms abroad, automation too has impacted new job creation. Other key industries like construction and business process outsourcing/IT enabled services too saw a 10% and 12% decline in hiring, respectively, showed the index... Meanwhile, city-wise, six out of eight metros saw a decline in hiring activity in April compared to a year ago. The hiring index for Delhi/National Capital Region, Mumbai, Chennai and Bengaluru saw a dip of 28%, 18%, 29% and 28%, respectively.

Staying on the topic of India's labour market,

Livemint raises doubts about the quality of the Quarterly Employment Survey (QES) of the Labour Bureau which captures data from establishments employing more than 10 workers. But the QES sample may be unrepresentative since more than 80% of its workers are regular and 96% are full-time, whereas the 2011 census data showed that 75% of workers nation-wide are employed for more than six months a year and the NSSO survey 2011-12 shows that only 18% of workers had regular wages or salaried employment.

10. Finally, on the new theory of financial markets by Andrew Lo, Adaptive Market hypothesis. Lo, one of the foremost critics of the efficient market hypothesis and its random-walk view of market movements, argues that the markets develop and adapt over time in an evolutionary manner. Lo calls human "rationalising beings" and not "rational beings". He

writes,

The Adaptive Markets Hypothesis is based on the insight that investors and financial markets behave more like biology than physics, comprising a population of living organisms competing to survive, not a collection of inanimate objects subject to immutable laws of motion. This simple truth has far-reaching implications. For one thing, it implies that the principles of evolution—competition, innovation, reproduction, and adaptation—are more useful for understanding the inner workings of the nancial industry than the physics-like principles of rational economic analysis. It implies that market prices need not always reflect all available information, but can deviate from rational pricing relations from time to time because of strong emotional reactions like fear and greed. It implies that market risk isn’t always rewarded by market returns. It implies that investing in stocks in the long run may not always be a good idea, especially if your savings can be wiped out in the short run. And it implies that changing business conditions and adaptive responses are often more important drivers of investor behavior and market dynamics than enlightened self-interest—the wisdom of crowds is sometimes overwhelmed by the madness of mobs.