In the context of the landmark US Supreme Court decision (see interactive graphic here) to uphold the right of Michigan's voters to ban racial preferences in college admissions, one which is certain to trigger calls for a roll-back of affirmative action policies in the US, The Century Foundation has a nice report on the striking levels of inequality in college admissions in the US. It writes,

While Asians attain a greater share of seats in four-year colleges than their proportion of population of 18 year-olds, African Americans and Hispanics constituted just 6 percent of the freshman classes of the 146 "most" and "highly" selective four-year colleges. African Americans and Hispanics were 15 and 13 percent, respectively, of all 18 year-olds in 1995. So blacks and Hispanics were considerably under-represented at these top schools even with affirmative action.

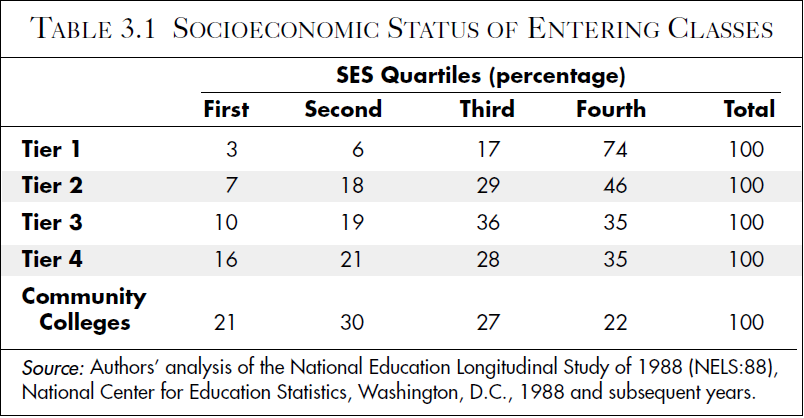

There is even less socioeconomic diversity than racial or ethnic diversity at the most selective colleges. Seventy-four percent of the students at the top 146 highly selective colleges came from families in the top quarter of the socioeconomic status scale (as measured by combining the family income and the education and occupations of the parents), just 3 percent came from the bottom socioeconomic status quartile, and roughly 10 percent came from the bottom half of the socioeconomic status scale. If attendance at these institutions reflected the population at large, 85000 students (rather than 17000) would have been from the bottom two socioeconomic quartiles.The findings of student distribution among the four different categories (classified on the SAT or ACT scores based admission criterion) of four-year colleges are shown in the table.

The figures are a graphic demonstration of why birth matters more than ever in determining life outcomes. If you have not been blessed by the ovarian lottery of taking birth in a richer family, then your likelihood of getting into one of the top colleges drops dramatically.