Matt Stoller points to a striking graphic from Sparkline Capital about the progressive market concentration in defence contracting market in the US.

From the end of the Cold War to the early 2000s, the number of prime contractors shrank from over 100 to 5, from a diverse set of actors to Boeing, Raytheon, Lockheed Martin, General Dynamics, and Northrop Grumman.

Policymakers in the Clinton administration also fostered contractor price gouging, especially on contracts where there was only one bidder, or ‘sole source’ contracts. A key way to do that was to eliminate contracting rules when buying things that were determined to be ‘commercial items.’ Originally meaning that contracting rules didn’t apply to things like pencils or off-the-shelf computers that are regularly sold to private citizens, Congress changed the meaning of ‘commercial items’ in the mid-1990s to mean anything, like military transports or sophisticated weapons system that are anything but commercial... For example, the C-130 transport - which has never been sold to a private commercial party - is considered a ‘commercial item.’ And its price, which should come down as technology and manufacturing know-how improves, has skyrocketed, from one model selling at $37.5 million in 1994 to a slightly bigger version going for $200 million apiece today...

TransDigm is a more blatant example. Transdigm is a company that bought up sole source providers of spare parts and raised prices; in one case they overcharged DoD as much as 4,451% on certain items. Indeed, according to the Pentagon’s inspector general, current regulations “enable sole-source providers and manufacturers of spare parts to avoid providing uncertified cost data, (which, if you want to get technical, is a much weaker and less reliable version of the certified cost data that contractors were routinely required to submit prior to the Clinton Administration’s embrace of defense contractors). Numerous government reports have repeatedly shown that the Pentagon pays too much for spare parts. For example, IGs found that companies charged DoD $71 for a pin that should have cost less than a nickel and $80 for a drainpipe segment that should have cost $1.41.

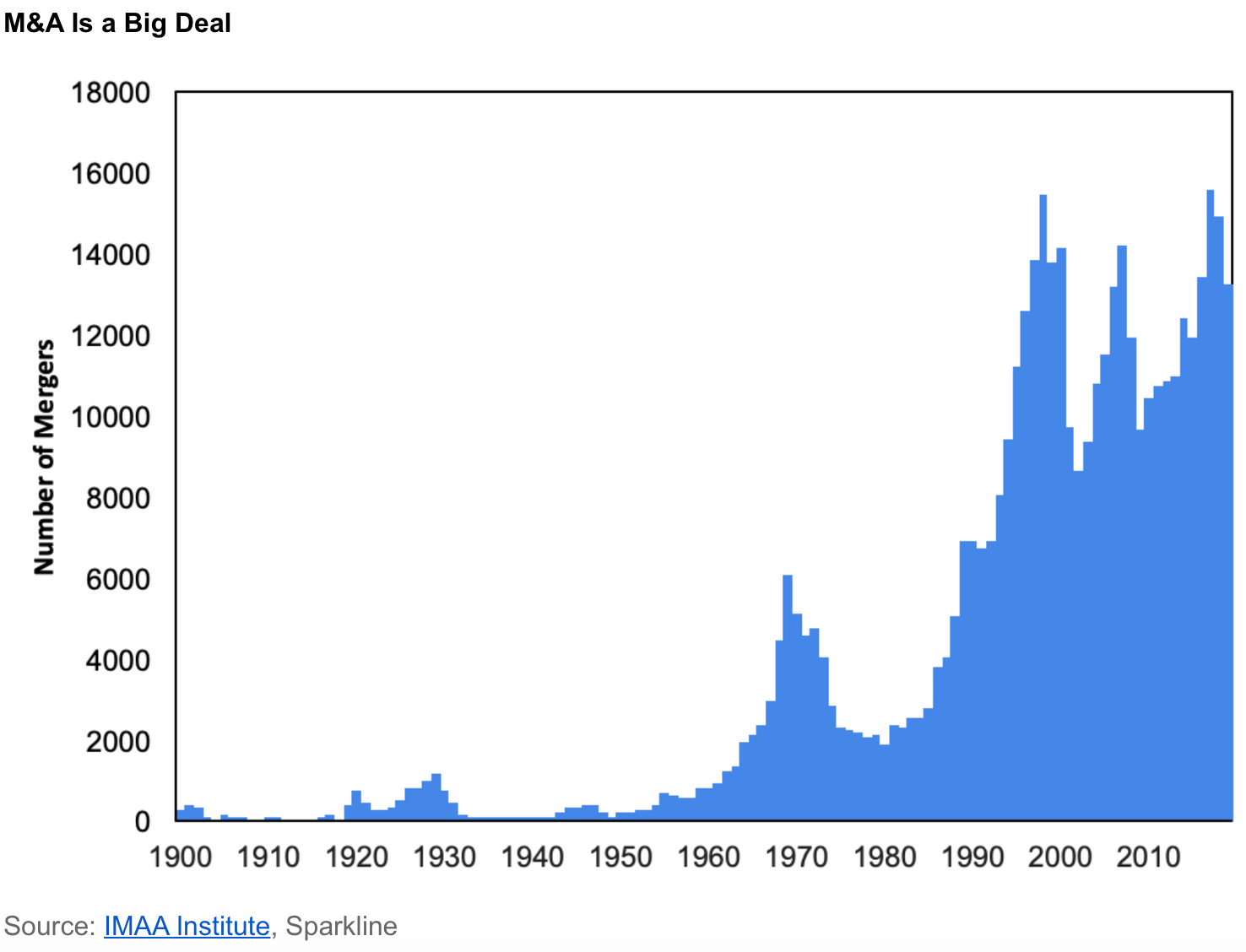

Sparkline Capital has a great read on the rise and consequences of monopoly capitalism. This from the airline industry, where by 2016 the big four airlines had an 80% market share.

This shows the market share in highly concentrated product markets

In general, David Autor and Co have shown that the market share in the US of the top four firms (superstar firms) in 676 industries increased by around 50% over the 1980-2012 period.

... and rely less on labour

Given their heavy use of automation, the labor efficiency of Big Tech is even more extreme. Apple only has 0.37 employees per $1 million revenue. Using this logic, Scott Galloway estimates that Google and Facebook’s disruption of the advertising industry led to around 199,000 job losses.

Expectedly, US corporate profit margins have risen sharply since the nineties

Historically, profits were reliably mean-reverting around 6% of GDP (blue). However, starting in the late-1990s, they seemingly underwent a paradigm shift (red). While they still gyrate with the business cycle, itappears to be around a significantly higher mean.

And this has been also associated with a decline in the share of income going to labour - both have been mirror images since 1997 or so.

Explaining this trend, Jose Azar et al examined over 8000 geographic-occupational labour markets in the US and found,

Based on the DOJ-FTC horizontal merger guidelines, the average market is highly concentrated. Using a panel IV regression, we show that going from the 25th percentile to the 75th percentile in concentration is associated with a 17% decline in posted wages, suggesting that concentration increases labor market power.And all through this period, anti-trust activity has been declining

Mergers are almost never blocked and companies are rarely fined for antitrust violations. The decline of antitrust enforcement has proceeded through both Democratic and Republican administrations.On a theoretical note, this early finding by Larry Summers and Brad De Long is spot on,

“An industry with high fixed costs and near-zero variable costs has another important characteristic: it tends to monopoly. The rule of thumb in high technology has been that the market leader makes a fortune, the first runner-up breaks even, and everyone else goes bankrupt rapidly. … [C]ompetition in already established markets with high fixed and low variable costs is nearly impossible to sustain.”

This is in addition to the conventional network effects.

The most disturbing factor is the political capture that invariably follows such business concentration. This, more than the business concentration by itself, is the corrosive aspect.

No comments:

Post a Comment