1. Vietnam's export machine gets a boost with the signing of an FTA with EU.

Once the agreement takes effect, 71 per cent of exports from Vietnam to the EU will become duty-free, as will 65 per cent of EU shipments to Vietnam. Of the remaining tariffs, up to 99 per cent will be phased out by Hanoi over 10 years and by Brussels over seven years... Once the deal takes effect, the bloc is to eliminate tariffs on 77.3 per cent of Vietnam’s textile and apparel exports after five years and the remaining 22.7 per cent after seven years.

Only makes India's attempts to attract global value chains from China that much harder.

2. The US and Europe have followed different stimulus approaches. The former adopted rolling out a generous unemployment benefit program that allowed businesses to furlough workers. The latter preferred to support firms with wage subsidy programs (like the German Kurzarbeit) to prevent firms from having to lay off workers. In a few months, we will be able to make an assessment of which approach was better at both limiting lockdown suffering as well as expediting recovery.

The Economist has an article that examines this dilemma.

3. This article about how Dharavi, with a population of 8.5 lakh, has keep its deaths to just 79. The number of tests done till now has been 7000 and the number of positive cases 2158.

Two things stand out clearly. One, with congested spaces and community toilets, it is inconceivable that since the first case was detected on April 1, the actual number of cases in Dharavi is just 2000 odd. Including all the asymptomatic cases, it is likely to be orders of magnitude higher. Then there has been the gradual lockdown easing. Despite all this, the number of deaths is just 79. This points to the lower fatality rates with the pandemic itself. Two, this has been achieved without the kind of mass testing that people demand as essential for addressing Covid 19.

These are the two headline points that I have been writing about in earlier posts. This is another story about Dharavi.

The decision to impose mandatory institutional quarantine in Delhi is completely unfounded on practical considerations and any professional opinion. This and this are good articles about reasons why it's just counterproductive.

4. The issue of reducing dependence on China has to start with defence requirements like protective gears. It is not enough to merely announce an intent to reduce dependence or even mandate that manufacturers don't source it from China. The issue of price competitiveness goes to the heart of most dependencies on China,

Neeraj Gupta, Managing Director of MKU, said the firm imports raw materials from either US or European countries which pushes their prices up. “Chinese raw materials are 60%-70% cheaper than other international firms but this is a sector where quality of the gear and minimum loss of life on the frontlines is of utmost importance,” he said.

It is also required to be willing to pay the higher price for equipment which is sourced from other countries or made locally. This will be the case for everything from solar power to telecommunications. Customers, including the government, should be willing to pay the higher price, atleast in certain strategic sectors.

As a policy, the Government of India should discourage Chinese companies from supplying to solar, thermal power, metro rail and railway, telecoms, and defence sectors. Also Chinese contractors should be barred from all construction projects. Finally, Chinese investments in tech companies should be disallowed. All these should be done directly or indirectly (visa restriction, technical specifications etc), as diplomatically feasible. The remaining sectors can be allowed to continue engagement without restrictions. The part of the 82 km Delhi-Meerut rapid rail project proposed to be awarded to Shanghai Tunnel Engineering Company could be the start.

But the boycott China policy has hard limits as Rathin Roy says,

We are not buying Chinese goods today out of any love for China. Why are even our sewing needles manufactured in China? We are not able to manufacture even low-end products as cheaply as China is. And therefore it is a rational economic decision to buy something from somewhere when it is sold as cheaply as possible. If you choose not to do that, then your economy becomes more expensive and then your growth falls, and you lose. You have two options. Either you accept that you are going to become a more expensive country, or you put in place a plan to produce the things you take from China, more cheaply in India. India has been in a situation where we can produce high-end products for our consumers, but when it comes to mass market items, we are uncompetitive, compared to other countries, not just China.

5. Good historical perspective on India-China border issue by Shyam Sharan here. More by him here on the need to exercise political control over the situation in the border. C Rajamohan writes about the need for a reset to India's China policy by acknowledging the rise of China and its expansionist ambitions. PJS Pannu on the undefined LAC. See also this by Nitin Gokhale. PB Mehta cautions against excessive reliance on outside help.

Good set of satellite images here about the activity at the LAC.

On the maritime side, in light of Chinese ports or refuelling facilities at Hambantota (Sri Lanka), Kyaukpyu and Sittwe (Myanmar), and Pyaara (Bangalodesh), the importance of securing the Bay of Bengal and Indian Ocean assumes critical importance,

But what happens if China insists that shipping liners should not travel into its extended nautical zone? Moves in southeast Asia suggest that it is prone to expansive notions of nautical boundaries. It will raise costs as ships take longer diversions. It can get worse if a nation follows up its warning with a possible disruption to even one commercial ship, claiming it an inadvertent strike. Costs for the nation will skyrocket, with not only longer shipping voyages but also added insurance costs.

The case for quick development of Andaman and Nicobar Islands as a military facility has never been more important.

6. A NAR article talks about Indian startups wooing Japanese investors. This can be a cautionary note,

Japanese companies have a rocky history of investing in India. Two major deals more than a decade ago -- Daiichi Sankyo's 500 billion yen (around $5.1 billion at the time) acquisition of pharmaceutical company Ranbaxy Laboratories in 2008 and NTT Docomo's 250 billion yen investment in a telecoms business of Tata in 2009 -- led to bitter legal disputes and are widely regarded as cautionary tales.

5. A status report on the only 24X7 water supply project under implementation in an Indian city, from Nagpur.

6. Tamal Bandopadhyay has a good article about the recent proposals by RBI to housing finance market. This summary of the market is useful,

The compounded annual growth rate of NBFCs in the five years between 2013 and 2018 was 17 per cent versus 9.4 per cent growth of the banking system; the HFCs grew even faster — 20 per cent. Since then, the HFCs’ growth has come down to around 13 per cent annually. There were 72 HFCs in 2015; since then the number has grown to nearly 100. As of December 2019, the size of the Indian housing finance market was Rs 20.7 trillion, including finance to commercial real estates and builders. The share of a few large banks, which have been aggressively chasing home buyers, is roughly two-thirds of this. One-third of this market belongs to the HFCs and NBFCs and about 10 of them have 90 per cent share of the pie.

7. Jahangir Aziz calls for cutting rates, increasing liquidity, and widening fiscal deficit in India.

8. Peter Navarro made a very valid point,

“One of the things that this crisis has taught us, sir, is that we are dangerously overdependent on a global supply chain for our medicines, like penicillin; our medical supplies, like masks; and our medical equipment, like ventilators.”

Martin Wolf disagrees branding it as protectionism. Both are talking past each other. Navarro is make the point in the context of the over-dependence on China. It is a case none of the liberals or opinion makers have made over the years as the world got sucked ever deeper into dependence on China. It took the Trump administration and renegades like Navarro to surface this concern. It cannot be anybody's cause that this state of affairs be continued.

Besides, and especially for larger economies and global powers like the US, resilience demands not just diversification away from China to other countries, but also some share of local production in atleast certain categories of products. If that requires reshoring, then so be it.

9. Austria issues a 2 billion euro 100 year bond with a yield of 0.88%. The bond was oversubscribed ten times!

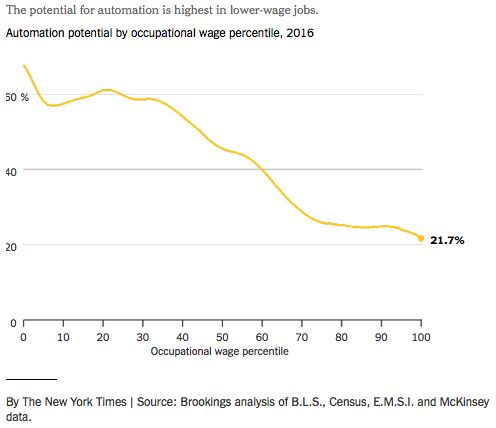

10. A NYT article about the low wage problem in the US economy. This graphic about how automation hits the low-wage jobs the most is instructive.

11. Roland Fryer has this summary of findings from his studies on racism in policing in the US. Yes, there is racism in non-lethal encounters, but not in shootings. And see also this by Coleman Hughes.

12. From a very nice NYT feature on ship-building in the US,

In the United States, large shipyards have been on the decline for decades, losing out on orders for massive commercial ships to cheaper foreign competition. Today, more than 90 percent of global shipbuilding takes place in just three countries: China, South Korea and Japan. What industry does remain in the United States is supported by the federal government, which orders American-made ships of all kinds, from Coast Guard cutters to naval aircraft carriers. The industry is also protected by a century-old law, the Jones Act, which requires that people and goods moving between American ports be carried on ships owned and operated by U.S. citizens and built domestically. The federal involvement has helped to preserve the vitality of the 124 remaining active American shipyards, which, according to government estimates, contribute more than $37 billion in annual economic output and support about 400,000 jobs.

13. Profile of the 3 million plus migrants who have returned to Uttar Pradesh post-lockdown. More than half are unskilled, with over half-a-million in construction.

14. Finally about the problems facing the start-up fund administered by SIDBI. The Fund of Funds initiated in 2016 with Rs 2500 Cr and a four-year commitment of Rs 10000 Cr. Till date, Rs 3798 Cr has been committed and Rs 1025 Cr drawn down. A Business Standard article writes,

Five years on, while the start-up fund has spurred some activity in the domestic VC ecosystem, the allocation from the fund has been slow and mired in bureaucratic hurdles, three investors concur. The process for sanction of funds takes months, or more. But an even bigger problem is that sanctions are typically contingent on the VC raising funds from other investors. For instance, if a VC with a Rs 100-crore targeted fund approaches Sidbi for a contribution of Rs 20 crore (20 per cent) and gets an approval, Sidbi could, in some cases, wait for the VC to raise the remaining Rs 80 crore before releasing the committed Rs 20 crore, says a Bengaluru-based investor closely involved with the bank. “Sidbi has made the fund-of-funds structure very convoluted,” says this investor. “It wants to be ‘last in, first-out’, does not allow tranche drawdown, and takes a long time to disburse the money. So, the investor’s hands are tied. If I get a good deal, I don’t have the money to invest,” the investor explains.

And this about the like problems with the Rs 10000 Cr government equity to a Rs 50000 Cr fund of funds to invest equity in SMEs,

Firstly, the structure of the fund envisages contribution by other investors as well — venture capitalists (VC), for example — but MSMEs are not a viable asset class for VCs to invest in. These companies do not offer the upsides that technology or technology-enabled businesses do, and that is one reason why there are no MSME-focused VCs, according to market participants. And secondly, even if the fund gets off the ground, the actual investment will not take place for six-eight months. By that time, most distressed small firms would have closed down.

No comments:

Post a Comment