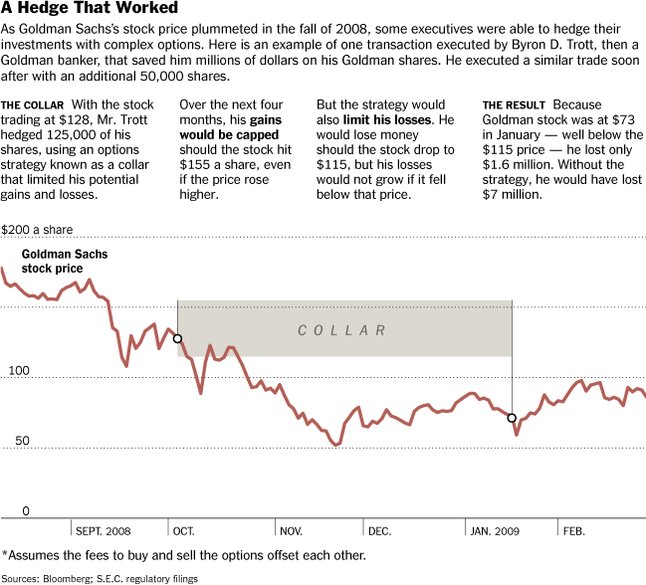

It now emerges that executives have been getting around this issue by hedging their downside on their holdings using complex investment transactions. Hedges allow employees to limit losses, raise cash, or diversify their portfolios without selling the underlying holdings. And no surprises for guessing who is leading the way - executives from Goldman Sachs (sample the Collar hedge below which while capping the potential upside also limits losses)!

Though most public companies, including Wall Street firms, have policies that ban hedging, albeit only their most senior executives, the practice is widespread at the lower levels. However, such hedges often put the executives interest in direct conflict with those of their company.

It is clear that reforming executive compensation is far from easy. Financial market reform is at best a moving target. Regulators and policy-makers have to be quick to respond to emergent distortions, if not be one-step ahead of the market. In practical terms, this means that instead of one-time enactments, they need to have legislations and rules that are constantly evolving in response to emergent scenarios.

No comments:

Post a Comment